Process Street has created this GRI 103: Management Approach 2016 Checklist Template, from the GRI Standards Management Approach report. The purpose of this template is to ease the efficiency and productivity of GRI reporting for your organization.

This checklist has features that work to lead you through the creation of your GRI report, ensuring that all information is recorded properly and that no steps are missed.

About GRI:103 Management Approach 2016 Standard

This GRI 103: Management Approach 2016 Standard is part of the set of GRI Sustainability Reporting Standards (GRI Standards). These Standards are designed to be used by organizations to report about their impacts on the economy, the environment, and society.

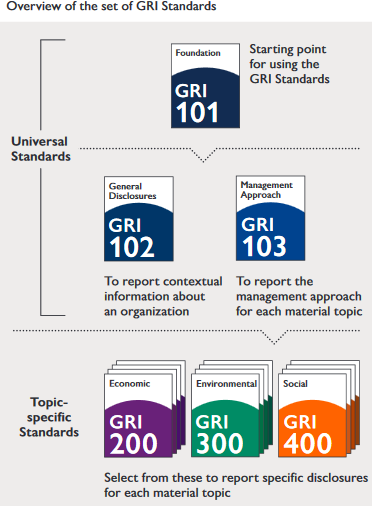

These GRI Standards are structured in a series of interrelated modules, that can be referenced and used together. The GRI 102: General Disclosure Standard is part of a set of universal standards that apply to every organization preparing a sustainability report:

- GRI 101: Foundation access our GRI 101: Foundation Template [HERE]

- GRI 102: General Disclosures

- GRI 103: Management Approach access our GRI:103 Management Approach [HERE]

When referencing the general standards, an organization can then look at the topic-specific GRI Standards for reporting on the material topics. These topic-specific Standards are organized into three series: 200 (Economic topics), 300 (Environmental topics) and 400 (Social topics). The image below details how these standards are organized.

Each topic Standard includes disclosures specific to that topic and is designed to be used together with the GRI: 103 Management Approach, which is used to report the management approach for the topic.

Using the GRI Standards and making claims

With two basic approaches of using the GRI Standards, there is a corresponding claim, or statement of use, which the organization is required to include in any published material.

1) The GRI Standards are to be used as a set to prepare the sustainability report following the Standards. The Standards can be prepared in accordance with Core or Comprehensive disclosures.

2) Selected GRI Standards, or part of their content, can be used to report on specific topics, without the use of the entire Standards. A GRI-referenced claim is used for published materials prepared in this way.

Background context

These management approach disclosures enable organizations to explain how they manage economic, environmental and social impacts. A narrative of information is provided of how the organization identifies, analyzes, and responds to its actual and potential impacts.

The disclosures about an organization's management approach give context for the information reported using topic-specific Standards (series 200, 300 and 400). This can be especially useful for the explanation of quantitative information to stakeholders.

Reporting requirements have a generic form and can be applied to a wide variety of topics. An organization preparing the report following the GRI Standards is required to report on its management approach for each material topic using this Standard. Additional reporting requirements, recommendations and/or guidance for reporting management approach information about the topic in question, are contained in topic-specific Standards.