''Economic growth and environmental protection are not at odds. They're opposite sides of the same coin if you're looking at longer-term prosperity.'' - Henry Paulson

Process Steet’s Environmental Accounting Internal Audit provides an easy-to-understand guide bringing forth an efficient and specialized performance analysis for a given small business. To reiterate, this performance analysis is ‘specialized’ as it abides by the practice of environmental management accounting.

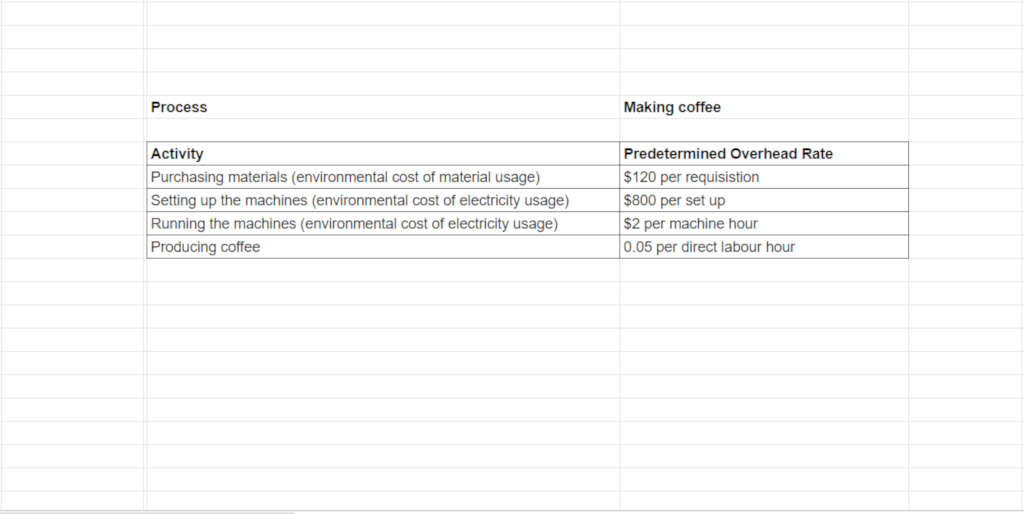

This means Process Steet’s Environmental Accounting Internal Audit solely considers environmental costs, such as the cost of energy, water, materials, waste and effluent disposal, in addition to indirect costs, such as environmental impacts on public image.

The Environmental Accounting Internal Audit aim is to identify costs, potential savings, to set targets and to monitor performance for a given small business specifically with an environmental focus.

Process Steet’s Environmental Accounting Internal Audit has condensed the environmental accounting as a procedure into the following tasks:

- Identify Environmental Costs

- Reduce Environmental Costs

- Produce An Action Plan

- Communicate Action Plan

- Assessment Of Targets

- Assess Benefits

Accounting as a practice was developed in the eighteenth century. The accounting profession has kept pace with the changing times, adapting to technological advances and advances in its study. Present-day accounting is more efficient and more precise, relative to its eighteenth-century version.

But today we face another change. Climate change and the loss of natural habitats and resources present a major risk to the global economy. For example, since 1980, extreme weather events have cost the U.S. $16 trillion.

As these changes to our natural world become increasingly acknowledged, actions to ameliorate this potential global crisis are far-reaching, impacting the niche discipline of accountancy.

Tax regime changes, changes in carbon trading and stricter regulations impact businesses at a financial level.

Accounting as a practice needs to take note, adapt and deliver the required long-term value. Accounting needs to adopt appropriate management of risk with sustainability as a fundamental key goal.

Process Steet’s Environmental Accounting Internal Audit has been designed to incorporate accountancy skills to help businesses deal with today’s unstable and changing environment.

For example, skills such as 'monitoring and reducing costs', 'helping to formulate and implement strategy', are applied in this internal audit.

Process Steet’s Environmental Accounting template manages environmental risks, saving you money, and supporting your small business to be sustainable.

In this template, you will be presented with specialized questions given as a form field. Different form fields are used, such as subtasks, dropdown menus, short answers, long answers, and weblinks.

You can populate each form field with your own specific data. This data is compiled to produce a report where appropriate.

In addition, our stop task feature has been used to enforce task order when needed. Our conditional logic task has been used as required to guide you through the correct process path specific for your entered data.