''Economic growth and environmental protection are not at odds. They're opposite sides of the same coin if you're looking at longer-term prosperity.'' - Henry Paulson

''Economic growth and environmental protection are not at odds. They're opposite sides of the same coin if you're looking at longer-term prosperity.'' - Henry Paulson

Process Steet’s Environmental Accounting Internal Audit provides an easy-to-understand guide bringing forth an efficient and specialized performance analysis for a given small business. To reiterate, this performance analysis is ‘specialized’ as it abides by the practice of environmental management accounting.

This means Process Steet’s Environmental Accounting Internal Audit solely considers environmental costs, such as the cost of energy, water, materials, waste and effluent disposal, in addition to indirect costs, such as environmental impacts on public image.

The Environmental Accounting Internal Audit aim is to identify costs, potential savings, to set targets and to monitor performance for a given small business specifically with an environmental focus.

Process Steet’s Environmental Accounting Internal Audit has condensed the environmental accounting as a procedure into the following tasks:

Accounting as a practice was developed in the eighteenth century. The accounting profession has kept pace with the changing times, adapting to technological advances and advances in its study. Present-day accounting is more efficient and more precise, relative to its eighteenth-century version.

But today we face another change. Climate change and the loss of natural habitats and resources present a major risk to the global economy. For example, since 1980, extreme weather events have cost the U.S. $16 trillion.

As these changes to our natural world become increasingly acknowledged, actions to ameliorate this potential global crisis are far-reaching, impacting the niche discipline of accountancy.

Tax regime changes, changes in carbon trading and stricter regulations impact businesses at a financial level.

Accounting as a practice needs to take note, adapt and deliver the required long-term value. Accounting needs to adopt appropriate management of risk with sustainability as a fundamental key goal.

Process Steet’s Environmental Accounting Internal Audit has been designed to incorporate accountancy skills to help businesses deal with today’s unstable and changing environment.

For example, skills such as 'monitoring and reducing costs', 'helping to formulate and implement strategy', are applied in this internal audit.

Process Steet’s Environmental Accounting template manages environmental risks, saving you money, and supporting your small business to be sustainable.

In this template, you will be presented with specialized questions given as a form field. Different form fields are used, such as subtasks, dropdown menus, short answers, long answers, and weblinks.

You can populate each form field with your own specific data. This data is compiled to produce a report where appropriate.

In addition, our stop task feature has been used to enforce task order when needed. Our conditional logic task has been used as required to guide you through the correct process path specific for your entered data.

In this Environmental Accounting Internal Audit, you will be presented with the following form fields, which you are required to populate with your own specific data. More information is provided for each form field via linkage to our help pages:

To begin the Environmental Accounting Internal Audit, enter the required details into the form fields below.

This is a stop task, which means you cannot progress in this environmental accounting internal audit until the required form fields are complete.

At certain points in this Environmental Accounting Internal Audit, results will need to be reviewed and approved by the relevant personnel within your team.

Take the time to fill in the details of the relevant personnel for audit review and subsequent approval below.

The first stage of Process Steet’s Environmental Accounting template consists of identifying environmental costs, both direct and indirect.

You are presented with Process Steet’s subtask form field. You can check off each task once it has been completed using this form field.

You are then presented with our website form field. Using this form field you can link online documents, such as a Google spreadsheet. You can use this website form field to record environmental costs identified.

In this case, you can link online documentation summarising information obtained from consulting the business ledger and supplier invoices (if required).

The dropdown form field presents a conditional step in this process. By selection 'Yes' or 'No' from the form field, you will be directed to the relevant stage in the process.

Make sure to identify the true value of environmental costs. Do not treat environmental costs as general overhead, as so commonly occurs. Instead, allocate each cost to individual products so as to not to distort the overhead.

You can do this using activity-based costing, which is covered in our 'Employ activity-based costing' task. To ensure that you are guided through the pathway that includes this task, choose 'Yes' from the dropdown form-field above.

This is a stop task, which means you cannot progress in this environmental accounting internal audit until the required form fields are complete.

The largest environmental costs are likely to include:

Check off each subtask once it has been completed.

You can then link online documentation summarising information obtained from meeting department managers and senior employees (if required).

This is a stop task, which means you cannot progress in this environmental accounting internal audit until the required form fields are complete.

For each individual process, speak to the relevant department managers and senior employees.

Department managers can provide more information in addition to information obtained from the business general ledger and supplier invoices. For example, department managers will know how long a given process takes. Time is a cost that must be included in environmental management accounts.

Causes or ''drivers'' of a cost associated with a specific activity are known as 'cost drivers'. For example, a cost driver could be the number of hours a machine has to run for a given activity to come to completion.

Check off each subtask once it has been completed.

You can then link online documentation summarising information obtained from meeting department managers (if required).

This is a stop task, which means you cannot progress in this environmental accounting internal audit until the required form fields are complete.

The activity-based costing system is not useful for companies with only one or two processes, which have little variation.

The below method to activity-based costing that has been interrupted from Managerial Accounting, Using Activity-Based Costing to Allocate Overhead Costs.

Environmental costs have already been identified in the previous tasks.

Cost of environmental processes has been identified in the task 'consulting the business ledger and supplier invoices'

If links to online documentation summarising the environmental process costs identified were provided, these links are presented below:

{{form.Online_documentation_URL_(1)}}

Environmental process costs have been broken down across different activities in tasks 'talking to senior employees and managers' and 'face-to-face meetings with department managers'.

If links to online documentation summarising the activity costs identified were provided, these links are presented below:

{{form.Online_documentation_URL_(2)}}

{{form.Online_documentation_URL_(3)}}

Overhead costs should have already been considered in tasks: 'consulting the business ledger and supplier invoices'; 'talking to senior employees and managers' and 'face-to-face meetings with department managers'.

The cost of resources for each product or activity needs to be allocated to that product or activity. Costs are assigned only to the products and activities that demanded that specific costly action.

Cost drivers should have already been considered in tasks: 'talking to senior employees and managers' and 'face-to-face meetings with department managers'.

You can then link online documentation summarising the calculated predetermined overhead rate (if required).

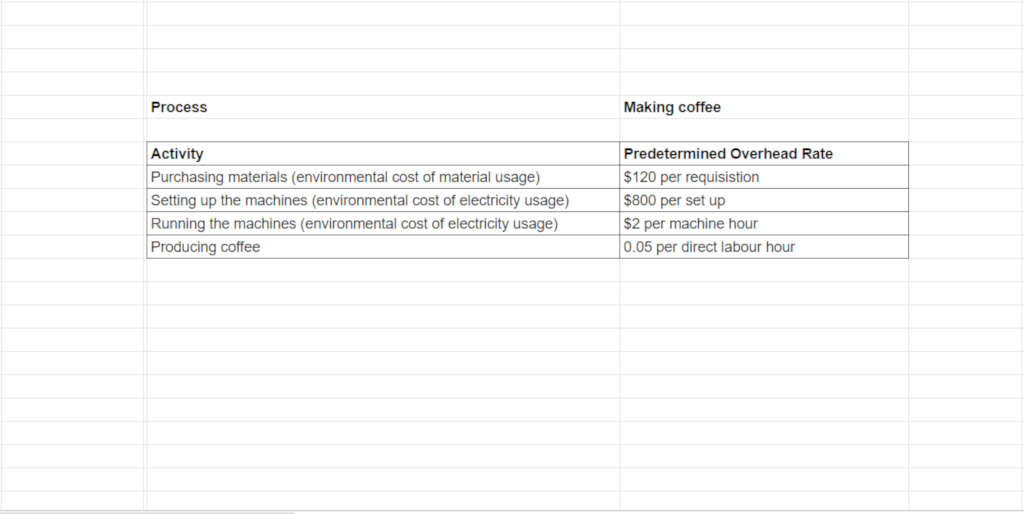

Indirect manufacturing costs are assigned to the goods that they produce via the predetermined overhead rate. The predetermined overhead rate is given as a cost per cost driver unit of measurement.

After a year of operation, actual cost driver activities can be determined from recorded data obtained in the operating year. So for example, the number of hours for a given activity might have been less in the year than previously estimated. You need to consider the actual cost drivers in step 5.

You can then link online documentation summarising the calculated applied overheads (if required).

Activity-based costing organizes activities into several cost pools, to allocate overhead costs. The idea is that the time, materials, and labor used to create a product or perform a given activity, are accounted for.

Companies using activity-based costing often identify hundreds of activities with costs associated.

It is important to be aware of the negatives associated with activity-based costing when consulting the applied overhead costs given:

Activity-based costing systems can be costly and time-consuming to implement. From identifying costs associated with activities to identifying the tracking cost drivers.

Using per unit cost information from activity-based costing does not account for fixed costs in the calculation. Fixed costs do not change in total with changes in activity.

The activity-based costing system is not useful for companies with only one or two processes, which have little variation. For example, if a company manufactures one product only, then overhead costs will be associated with the manufacture of that one produce.

The summary of activity-based costing results detailed below, need to be reviewed and approved by the relevant personnel before continuation of this Environmental Accounting Internal Audit is possible.

Environmental costs of each process have been identified during the task 'consulting the business ledger and supplier invoices'.

If a link to online documentation summarising these costs identified was provided, this link is presented below:

{{form.Online_documentation_URL_(1)}}

Environmental costs for each process were broken down across different activities and cost drivers associated with each activity were identified.

If a link to online documentation summarising these costs identified was provided, this link is presented below:

{{form.Online_documentation_URL_(2)}}

{{form.Online_documentation_URL_(3)}}

Predetermined overhead rate for each activity was calculated.

If a link to online documentation summarising these predetermined overhead rates was provided, this link is presented below:

{{form.Online_documentation_URL_(4)}}

Applied overhead costs have been calculated and assessed to be identified as overapplied or underapplied.

If a link to online documentation summarising these overhead rates was provided, this link is presented below:

{{form.Online_documentation_URL_(5)}}

The largest environmental costs are likely to include:

Waste and effluent disposal

Water consumption

Energy

Transport

Consumables and raw materials

Begin your cost reduction analysis identifying true costs associated with waste. Check off the subtasks when each has been explored.

A long text form field is provided for you to summarize the target activities identified for environmental cost reduction or elimination.

For more information on reducing and managing waste, view the following guides:

Quick links to these guides are provided below:

Identify true costs associated with water consumption. Check off the subtasks when each has been explored, and populate the long text form field as required.

Mains water supply charges are rising on a global scale along with sewage and trade effluent charges. Controlling water supply is therefore important.

To find out how to monitor your waste use, consider the following guides:

For information on how to save water, view the following guides:

Quick links to these guides are provided below:

Identify true costs associated with energy consumption. Check off the subtasks when each has been explored, and populate the long text form field as required.

Government initiatives and grants encourage energy efficiency. For more information, see the following guide:

For more information on how to save money by being more energy efficient, see the following guide:

Quick links to these guides are provided below:

Identify true costs associated with transport. Check off the subtasks when each has been explored, and populate the long text form field as required.

For more information on how to implement the above, see the following guides:

Quick links to these guides are provided below:

Identify true costs associated with consumables and raw materials. Check off the subtasks when each has been explored, and populate the long text form field as required.

For more information regarding the above, see the following guide:

Quick links to these guides are provided below:

The dropdown form field represents a conditional step in this template. Selecting 'Yes' or 'No' from the dropdown menu will lead you to the relevant pathway in your active checklist.

The processes specifically considered, named below, are processes most likely to have the largest environmental costs associated.

However, there may be other processes not considered in this Environmental Accounting template with environmental costs associated that need to be considered.

Take the time to work through true environmental costs not already considered and identify possible cost reductions and eliminations. Summarize these additional target activities in the long text form field below.

Summarized target activities need to be reviewed and approved before the completion of this Environmental Accounting Internal Audit.

In the dropdown form field below, you have the option to send this summary report to relevant stakeholders. The dropdown form field is a conditional step. Selecting 'Yes' or 'No' from the dropdown menu will lead you to the relevant pathway in your active checklist.

The summarized activities identified as targets to reduce and/or eliminate environmental costs need to be reviewed and approved by the relevant personnel before the completion of this internal audit.

{{form.Waste_production_and_disposal:_summarize_target_activities_identified_for_cost_reduction_or_elimination}}

{{form.Water_consumption:_summarize_target_activities_identified_for_cost_reduction_or_elimination}}

{{form.Energy_consumption:_summarize_target_activities_identified_for_cost_reduction_or_elimination}}

{{form.Transport:_summarize_target_activities_identified_for_cost_reduction_or_elimination}}

{{form.Consumables_and_raw_materials:_summarize_target_activities_identified_for_cost_reduction_or_elimination}}

{{form.Summarize_target_activities_identified_for_cost_reduction_or_elimination_that_have_not_yet_been_considered}}

Targets need to be reviewed and approved by the relevant personnel for the continuation of this Environmental Accounting Internal Audit.

Check your set targets to ensure the following have been considered:

Your changes to reduce environmental costs and to employ more sustainable actions in your business will have immediate or delayed costs savings.

Take the time to estimate the cost savings you will achieve and to estimate payback periods of any investments made.

All relevant departments will need to assess their progress towards achieving the set targets. For this assessment, ensure that periodic reports are produced, reporting on the department's progress.

Our dynamic due date feature has been implemented on this step to ensure that periodic reports are assessed in a months time.

Check off each subtask on its completion.

You are presented with a conditional step. Selecting 'Yes' or 'No' in the drop-down menu given will direct you to the relevant pathway in this process.

Produce a flow chart to show the businesses main activities. Include the following in this flow chart:

{{form.Based_on_the_activities_identified_to_reduce_or_eliminate_environmental_costs,_formulate_target_for_environmental_cost_reduction/elimination.}}

The flow chart should not be overly detailed but should show the key information where you can make savings.

Communication is important to ensure that employees are enthusiastic and knowledgeable about the given changes. Flow charts have visual clarity meaning multiple processes and associated activities can be viewed easily in a single document, making it an excellent way to communicate the changes required from running this checklist.

You are presented with a conditional step. Selecting 'Yes' or 'No' in the drop-down menu given will direct you to the relevant pathway in this process.

{{form.Based_on_the_activities_identified_to_reduce_or_eliminate_environmental_costs,_formulate_target_for_environmental_cost_reduction/elimination.}}

This is a stop task. Completing the Environmental Account Internal Audit is not possible until all targets have been met.

Continuation of the assessment tasks is required until all targets have been met.

This is a stop task, which means you cannot progress in this environmental accounting internal audit until the required form fields are complete.

The conclusion put forward in regard to whether every target has been met needs to be reviewed and approved by the relevant personnel before the continuation of this Environmental Accounting Internal Audit is possible.

You can document your cost savings achieve in an online document and provide the URL link.

Alternatively, you can upload a file summarizing the savings achieved.

Financial and Environmental benefits detailed need to be reviewed and approved by the relevant personnel before these benefits can be emailed to the relevant personnel.