Turn every policy into automated workflows with built-in enforcement and audit-ready proof.

Internal Controls

Internal controls are the policies, procedures, approvals, reviews, checks, and workflows that help an organization prevent mistakes, detect problems, correct issues, and prove that work was done properly.

They matter because businesses do not run on intent. They run on repeatable actions. If a payment can be approved by the wrong person, if evidence is collected after the fact, or if exceptions disappear into email, the control environment is weak even when the policy looks good.

This guide explains what internal controls are, why they matter, the main control types, examples by team, how controls work in practice, and how to turn controls into auditable workflows.

In this article, we are going to cover:

- What are internal controls?

- Why internal controls matter

- What internal controls include

- Types of internal controls

- How internal controls work in practice

- Internal control examples by team

- How Process Street supports internal controls

- FAQs

What are internal controls?

Internal controls are the mechanisms an organization uses to guide work, reduce risk, protect assets, keep records accurate, and prove accountability. The concept is common in finance, audit, compliance, operations, IT, HR, procurement, and quality management.

COSO guidance on internal control is one of the most recognized references for internal control. The model frames internal control as a system involving governance, risk assessment, control activities, information and communication, and monitoring.

The GAO Standards for Internal Control in the Federal Government applies a similar idea in the public sector: controls are not a single checklist. They are a system of policies, roles, activities, evidence, and monitoring that helps an organization achieve objectives.

For public companies, the SEC management report on internal control over financial reporting shows how internal control over financial reporting connects management responsibility, disclosure, and evidence.

Internal controls are active, not decorative

A control is only useful when it changes behavior. A policy that says expenses need approval is not enough. The control is the approval workflow that blocks payment until the right reviewer approves, records the decision, and stores proof.

Strong controls live inside the way work happens. They make the correct path easy, make risky shortcuts visible, and preserve the evidence needed for audit, compliance, and management review.

This is why internal controls should be described in operational terms. Instead of saying that the company has a vendor control, define the exact trigger, the person or system responsible, the evidence required, the approval path, and the exception rule. A reviewer should be able to follow the control from start to finish without guessing how the work is supposed to happen.

Internal controls and compliance

Internal controls are a core part of compliance operations because they connect requirements to execution. Regulations, standards, contracts, and internal policies all depend on controls that can be performed, tested, and improved.

The same logic applies outside regulated teams. Operations teams use controls to standardize handoffs. HR teams use controls to confirm training and policy acknowledgment. IT teams use controls to manage access. Finance teams use controls to protect cash and reporting accuracy. The control environment is the shared structure that lets these teams operate with confidence.

Why internal controls matter

Internal controls matter because organizations scale faster than informal trust. In a small team, people can remember who approves what and where proof lives. In a larger business, that memory breaks. People change roles, systems multiply, regulations tighten, and exceptions become harder to see.

Controls create a stable operating system for risk. They define what should happen, who owns it, what evidence proves it happened, what happens when it fails, and how leadership knows the system is working.

They protect the business

Internal controls protect cash, data, inventory, intellectual property, customer records, employee information, financial reports, regulated processes, and brand trust. A missing control can create loss, fraud, misstated reporting, failed audits, data exposure, or operational disruption.

They make accountability visible

Good controls make ownership explicit. That is also why internal audit and operational audit depend on clear control owners, evidence trails, and exception handling. The audit is easier when the work already produced proof.

They reduce audit fire drills

When controls run inside documented workflows, teams do not need to reconstruct proof weeks or months later. The workflow itself becomes the source of evidence. That is the core idea behind compliance as proof of control: proof should come from execution, not from a last-minute evidence chase.

They make growth less fragile

Internal controls also make growth less fragile. New hires can follow a defined process. New locations can inherit the same review pattern. New systems can be connected to existing approval and evidence requirements. Without controls, growth creates more exceptions, more informal workarounds, and more knowledge trapped in individual inboxes.

A mature control environment does not mean every action needs heavy approval. It means the organization knows which risks matter, which controls are worth enforcing, and which low-risk steps can stay lightweight. That balance keeps teams moving while still protecting the business.

The goal is consistent control without unnecessary friction.

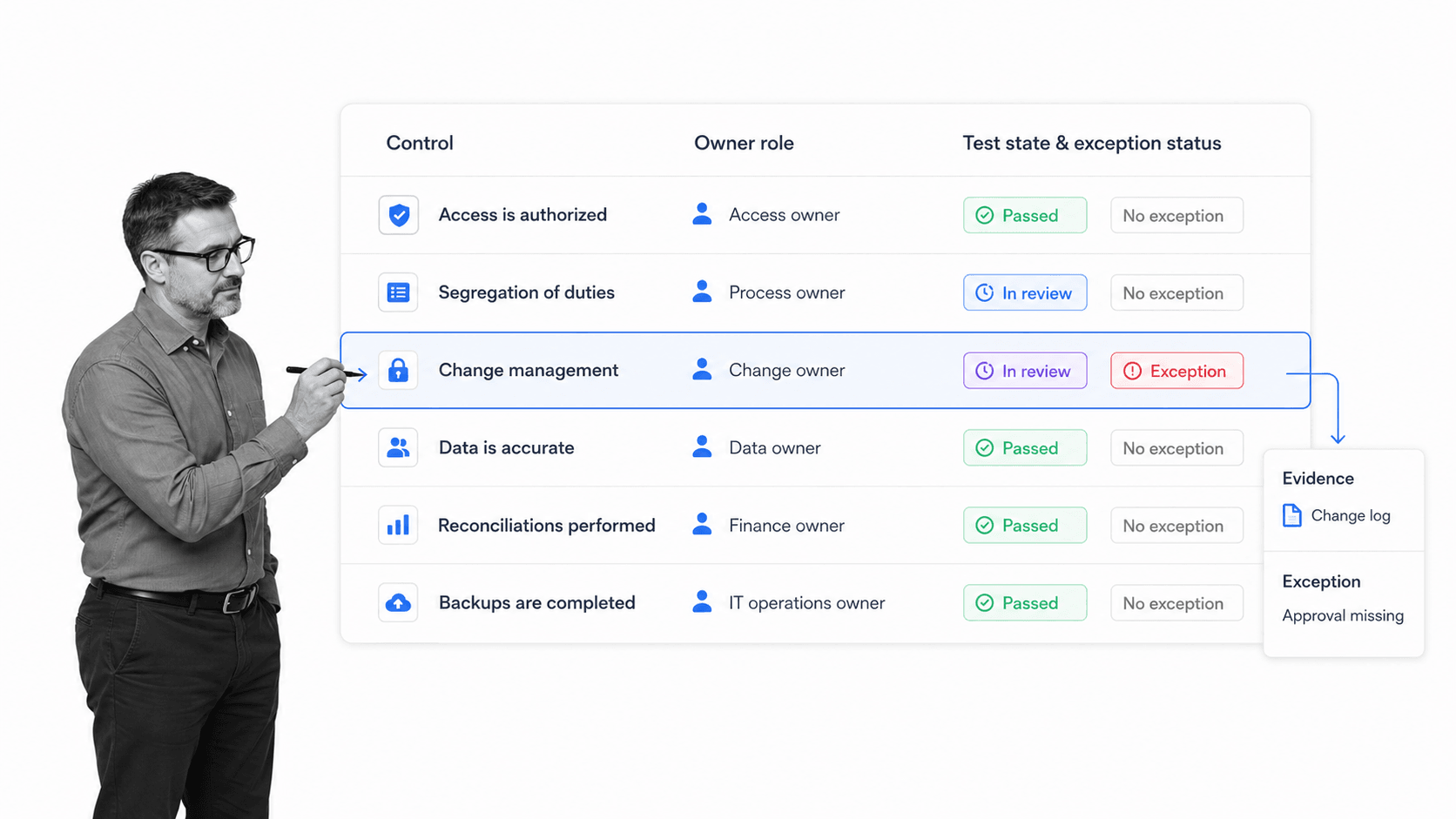

What internal controls include

Internal controls include the structure around a control and the activity itself. A useful control record should tell a reviewer what risk the control addresses, who owns it, how often it runs, what evidence is required, and what happens when the control fails.

Control objective

The control objective explains why the control exists. For example, the objective might be to prevent unauthorized payments, detect duplicate vendors, ensure access reviews happen on schedule, or confirm a regulated procedure was followed.

Control activity

The control activity is the actual thing performed: approval, reconciliation, review, segregation of duties, access check, policy acknowledgment, exception review, evidence upload, system validation, or signoff.

Owner, frequency, and evidence

Every control needs an owner. It also needs a frequency, such as per transaction, daily, monthly, quarterly, annually, or event-based. The evidence requirement should be specific enough that a reviewer can tell whether the control ran as intended.

Controls also need supporting document discipline. document control best practices and policy management software help because uncontrolled documents create uncontrolled execution.

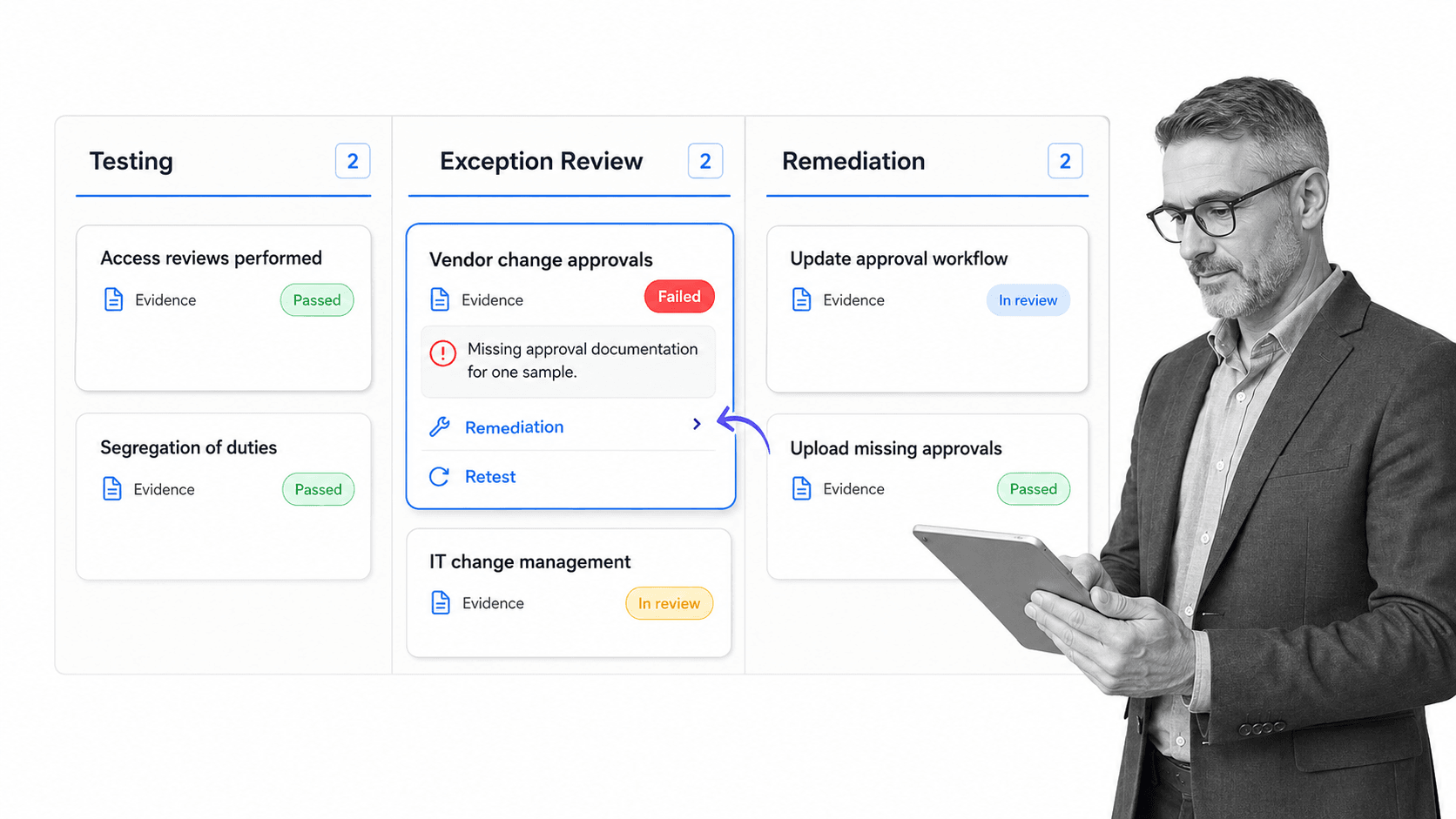

Exception and remediation path

A control that fails without a remediation path is incomplete. The control record should specify how exceptions are logged, who reviews them, how remediation is assigned, what evidence closes the issue, and whether retesting is required.

Control documentation

Control documentation should be plain enough for the control owner to perform the activity and precise enough for an auditor to test it. At minimum, document the control objective, risk, owner, frequency, steps, evidence, system of record, reviewer, exception path, and retention requirement.

Avoid vague wording such as review periodically or attach documentation. Replace it with operational language: review the access report every month, confirm each user still needs access, upload the completed review file, route exceptions to the system owner, and record removal evidence before closing the task.

Types of internal controls

Internal controls are often grouped by when they act and what they protect. The three most common timing categories are preventive, detective, and corrective controls.

The AICPA internal control resources also frames internal control as a management responsibility that supports reliable operations, reporting, and compliance.

Preventive controls

Preventive controls stop a problem before it happens. Examples include approval gates, access restrictions, required fields, segregation of duties, spending limits, training acknowledgments, locked templates, and system validations.

Detective controls

Detective controls identify a problem after activity occurs. Examples include reconciliations, variance reviews, exception reports, access review reports, inventory counts, log monitoring, quality checks, and internal audits.

Corrective controls

Corrective controls fix the issue and reduce the chance it happens again. Examples include remediation workflows, policy updates, retraining, access removal, process redesign, escalation, root cause analysis, and retesting.

Manual and automated controls

Manual controls rely on people performing and recording work. Automated controls rely on systems to enforce rules or capture evidence. Most organizations need both. The key is knowing which controls are high risk, which can be automated, and which need human judgment.

Teams often begin with a risk assessment template, then build repeatable control workflows as they learn which risks need stronger enforcement.

Entity-level and process-level controls

Entity-level controls shape the overall control environment. Examples include board oversight, ethics policies, risk governance, delegation of authority, and management review. Process-level controls operate inside a specific workflow, such as procure-to-pay, hire-to-retire, incident response, or financial close.

Both levels matter. Entity-level controls set expectations, but process-level controls prove whether work is happening correctly. A company can have a strong code of conduct and still fail if access reviews, payment approvals, or quality checks are not performed and evidenced.

How internal controls work in practice

Internal controls work in practice through a cycle: define the risk, design the control, assign ownership, execute the control, collect evidence, test the result, remediate exceptions, and monitor performance over time.

Design the control around a real risk

A control should not exist because a spreadsheet has an empty row. It should exist because a real risk needs a repeatable response. Start with the risk, then define the control objective and activity.

Put the control where work happens

The best control is embedded in the workflow. If a finance manager approves payment, the approval should happen before payment. If a new vendor needs screening, the screening should happen before vendor activation. If a policy needs review, the review should trigger before the policy expires.

Test controls with evidence

Control testing checks whether the control is designed well and operating effectively. The test should inspect evidence, not intentions. An internal audit checklist template, financial audit checklist template, and clear audit procedures can help teams standardize that review.

Monitor and improve

Control monitoring turns one-time review into continuous improvement. Leaders should know which controls are overdue, which fail repeatedly, which exceptions remain open, and which procedures need redesign. This is where AI-driven compliance can help surface risk patterns, but ownership and workflow design still matter.

In Sarbanes-Oxley programs, Sarbanes-Oxley section 404 overview is one common reference point for why control documentation, management assessment, and testing discipline need to stay connected.

Keep the control owner close to the process

Control owners should be close enough to the work to know whether the evidence is meaningful. If the owner only updates a spreadsheet after the fact, the control is more likely to drift. Build the control into the operational workflow so the owner can complete, review, and correct the activity while the context is still fresh.

The same principle applies to control testing. Testers need a clear population, sampling method, evidence trail, and exception definition. If those pieces are vague, testing becomes a debate about interpretation instead of a review of whether the control operated effectively.

Internal control examples by team

Internal control examples are easiest to understand by department. The exact control depends on the risk, but the pattern is consistent: define the required action, enforce ownership, capture evidence, and review exceptions.

Finance controls

- Require approval before payments above a threshold.

- Separate vendor creation from payment approval.

- Reconcile bank activity against accounting records.

- Review unusual journal entries before close.

- Attach invoice, approval, and payment evidence to the transaction record.

IT and security controls

- Review user access on a recurring schedule.

- Remove access when employees change roles or leave.

- Require approval for privileged access.

- Monitor system logs for suspicious activity.

- Document incident response steps and evidence.

HR and operations controls

- Require policy acknowledgment during onboarding.

- Use checklists for regulated employee training.

- Route exceptions to the right reviewer before work continues.

- Track certifications, licenses, and required renewals.

- Standardize handoffs for recurring operational processes.

Procurement and vendor controls

- Screen new vendors before approval.

- Require independent review before vendor banking details change.

- Match purchase order, receipt, and invoice evidence before payment.

- Review contract renewals before automatic renewal dates.

- Escalate vendor exceptions before work or payment proceeds.

Quality and compliance controls

- Use approved procedures for regulated work.

- Require evidence before a quality review can close.

- Route nonconformances to corrective action owners.

- Confirm required documentation is current before release.

- Retain review history for audit and certification needs.

These examples connect directly to risk management. Risk is not reduced by naming it. Risk is reduced when the control is performed, reviewed, and improved.

How Process Street supports internal controls

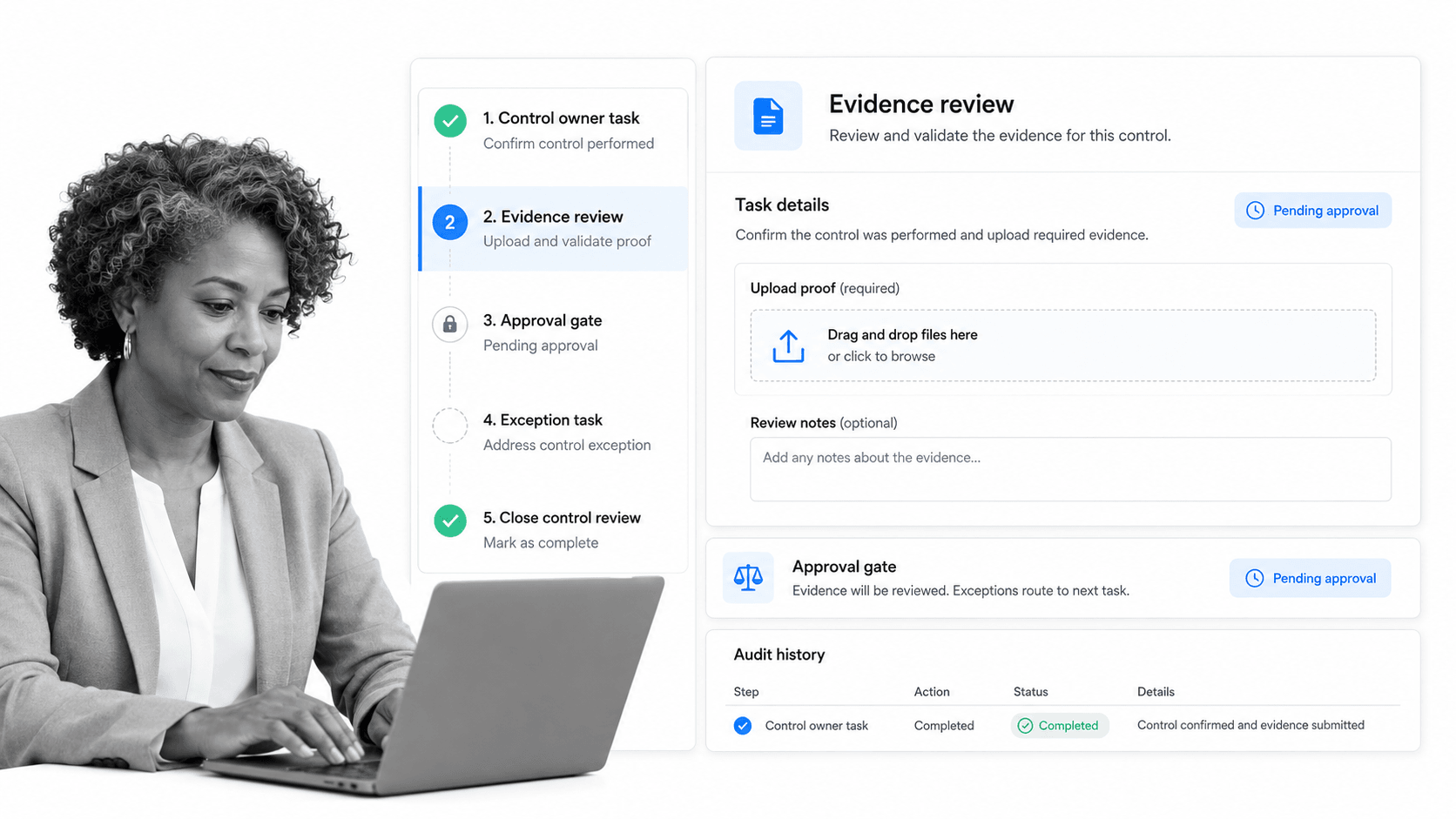

Process Street is a Compliance Operations Platform. It helps teams turn internal controls into recurring workflows with assigned owners, required evidence, approval gates, conditional paths, automations, and audit history.

That matters because internal controls usually fail at the execution layer. The policy says a review should happen, but the review is late. The control owner performs the work, but the evidence is missing. The exception is noticed, but remediation is not assigned. The audit asks for proof, but the proof is scattered across systems.

Controls become executable workflows

With Process Street, a control can run as a workflow. Required tasks, form fields, file uploads, due dates, assignments, approvals, and conditional logic make the control harder to skip and easier to prove.

Evidence is captured during the work

Evidence should not be a separate project. It should be created by the workflow that performs the control. When a task is completed, a file is uploaded, a reviewer approves, or an exception is routed, the activity history becomes part of the audit trail.

Exceptions get a closed-loop path

Internal controls are strongest when exceptions have a defined path. A failed review should create an owner, a due date, a remediation task, and a retest requirement. That turns control failure into managed work instead of a note that disappears after the review meeting.

The system can connect to the rest of your stack

Process Street has direct, universal integrations to 5,000+ systems. Need a new one? An AI agent builds it on the fly. That lets teams connect control workflows to the systems where financial records, employee records, vendor data, tickets, documents, approvals, and evidence already live.

For teams moving from static compliance documentation to operational control, digital compliance officer is the natural next step: a control layer that monitors, routes, and escalates work before risk becomes an audit finding.

FAQs

What are internal controls?

Internal controls are the policies, procedures, approvals, reviews, checks, workflows, and evidence requirements that help an organization prevent mistakes, detect issues, correct problems, and prove accountability.

What are the main types of internal controls?

The main types of internal controls are preventive controls, detective controls, and corrective controls. Preventive controls stop problems before they happen, detective controls find problems after activity occurs, and corrective controls fix the issue.

What are examples of internal controls?

Examples of internal controls include approval gates, segregation of duties, access reviews, reconciliations, required evidence uploads, policy acknowledgments, exception reports, audit trails, and remediation workflows.

Who is responsible for internal controls?

Management owns the design and operation of internal controls, but control responsibility is distributed across teams. Control owners perform the activity, reviewers test evidence, and leaders monitor whether the system works.

How do you test internal controls?

Test internal controls by checking whether the control is designed to address the risk and whether it operated as intended. Review evidence, sample completed work, inspect approvals, confirm exceptions were handled, and document any remediation.

How does Process Street help with internal controls?

Process Street helps teams turn internal controls into executable workflows. It assigns owners, enforces required steps, collects evidence, routes approvals, tracks exceptions, and preserves audit history as the work happens.