Turn every policy into automated workflows with built-in enforcement and audit-ready proof.

Hedge Fund Processes

Hedge fund processes are the repeatable workflows a fund uses to turn investment decisions into controlled execution, clean records, investor communication, and audit-ready proof. They cover front office work such as idea generation and trading, middle office work such as risk and reconciliation, and back office work such as fund accounting, compliance, and reporting.

A hedge fund can have a strong strategy and still create operational risk if the process layer is weak. Missed approvals, stale policies, late reconciliations, unclear ownership, and informal handoffs can turn routine work into regulatory exposure or investor distrust.

This guide breaks down the core hedge fund processes, shows how they connect, and explains how to document them in a way that operators, compliance teams, and leadership can actually use.

In this article, we are going to cover everything you need to know about hedge fund processes, including:

- What are hedge fund processes?

- Why hedge fund processes break down

- Core hedge fund process areas

- Hedge fund compliance processes

- Hedge fund risk and control processes

- How to document hedge fund processes

- How to improve hedge fund processes with automation

- Hedge fund process checklist

- Hedge fund processes FAQs

What are hedge fund processes?

Hedge fund processes are the operating routines that keep a fund investable, controlled, and explainable. They define who does the work, which inputs are required, which approvals must happen, what evidence is retained, and what happens when an exception appears.

The term matters because hedge funds are not just portfolios. They are operating companies with investment, legal, finance, technology, investor relations, and compliance work happening at the same time. Investor.gov describes hedge funds as private investment funds that pool investor money and invest in securities or other assets, which means the process layer has to support both investment activity and investor obligations.

In practice, hedge fund processes usually fall into three connected layers:

- Front office processes: idea generation, research, portfolio construction, trade approval, and order placement.

- Middle office processes: trade capture, allocation, risk monitoring, position checks, valuation support, and reconciliations.

- Back office processes: fund accounting, NAV support, investor reporting, tax coordination, compliance records, and audit preparation.

The best process designs connect those layers instead of treating them as separate departments. A trade idea should produce an approved order, an executed trade should produce a reconciled position, and a reconciled position should feed reporting, risk review, and books and records.

That is where Process Street fits for operations and compliance teams. A recurring process can run as a governed workflow, with assigned owners, required evidence, approvals, conditional logic, and audit trails tied to the work itself.

A process is not the same as a policy

A policy says what must be true. A process makes it happen. For example, a personal trading policy may say employees must pre-clear trades. The process defines the form, approver, restricted list check, exception path, evidence retention step, and escalation if an approval is missing.

A process is not the same as a checklist

A checklist is useful, but a hedge fund process needs ownership, timing, controls, system handoffs, approvals, and evidence. A simple list of tasks can help a small team remember steps. A controlled process helps the firm prove the right steps happened.

Why hedge fund processes break down

Hedge fund processes usually break down because the work crosses systems and teams. A portfolio manager may start the activity, operations may capture it, finance may reconcile it, compliance may review it, and investor relations may explain the result. If each team works from its own spreadsheet, inbox, or memory, the fund loses control at the handoff points.

The common failure modes are predictable:

- Unclear ownership: everyone knows the task matters, but nobody owns the next step.

- Informal approvals: decisions happen in chat or email, then become hard to reconstruct later.

- Manual exception tracking: breaks, missing documents, and valuation questions sit in spreadsheets with no escalation path.

- Policy drift: the written procedure changes, but the daily workflow does not.

- Evidence gaps: the work was done, but the fund cannot quickly prove who did it, when, and against which standard.

The stakes are higher in regulated investment environments because the process record often matters as much as the outcome. Rule 206(4)-7 under the Investment Advisers Act, for example, requires registered advisers to adopt written compliance policies and procedures and review them no less frequently than annually. That requirement is not just a document task. It depends on a working process for policy ownership, implementation, review, evidence, and remediation.

Strong hedge fund processes reduce that dependency on memory. They turn recurring work into a system: triggered, assigned, reviewed, measured, and retained.

The hidden risk is process variance

Most teams can describe the right process in a meeting. The problem is whether the same process happens the same way under pressure. Month-end close, investor requests, SEC exam preparation, new account opening, and trade breaks all create time pressure. Under pressure, people skip steps unless the workflow enforces them.

The fix is not more documentation

More documentation can make the problem worse if it creates another static file to maintain. The fix is to connect procedure, execution, evidence, and review. That means the SOP should not sit apart from the work. It should drive the work.

Core hedge fund process areas

Every hedge fund is different, but most funds need process discipline across the same operating categories. The mix depends on strategy, asset class, jurisdiction, investor base, service providers, and internal staffing model.

Investment research and idea review

The research process defines how ideas are sourced, screened, documented, challenged, approved, and monitored. A strong process captures the thesis, expected risk, data sources, conflict checks, and decision record. It also defines what changes after the position is live: review cadence, stop conditions, risk limits, and exit triggers.

For funds that need a structured research workflow, a checklist for investment analysis can turn ad hoc research into a repeatable decision record.

Trade approval and execution

The trade process connects the investment decision to execution. It should define order creation, approvals, restricted list checks, allocation rules, broker selection, best execution review, and post-trade capture. The process should also define who resolves rejected trades, allocation breaks, late confirms, and settlement exceptions.

Portfolio and risk monitoring

Risk monitoring is not a dashboard alone. It is a process for identifying exposures, reviewing limits, escalating breaches, documenting decisions, and confirming remediation. This may include market risk, liquidity risk, counterparty risk, concentration risk, leverage, operational risk, and model risk.

The broader risk management process needs clear triggers and owners. The hedge fund version should connect exposure monitoring with investment committee records, portfolio manager responses, and evidence for later review.

Trade capture, reconciliation, and exception handling

Operations teams need a tight process for trade capture and reconciliation because every downstream record depends on it. Positions, cash, P&L, fees, margin, investor reports, and financial statements all rely on clean data. A reconciliation process should define sources, timing, tolerances, exception severity, owner assignment, and closure evidence.

Fund accounting and NAV support

Fund accounting processes coordinate the data needed to calculate and validate NAV. That includes trade files, cash movements, accruals, expenses, management and performance fees, pricing inputs, valuation support, and administrator review. Even when a third-party administrator performs the calculation, the manager still needs a process for review, challenge, approval, and investor communication.

Fund administration providers often describe accounting, financial reporting, regulatory compliance, capital activity, and investor services as core administrative duties. The manager’s internal process should make those external handoffs visible and controlled.

Investor onboarding and investor relations

Investor-facing processes include subscription document collection, AML/KYC checks, accredited investor or qualified purchaser evidence where applicable, side letter tracking, capital activity, investor updates, and request handling. Investor relations work also needs a record of what was sent, when, to whom, and with which approvals.

The investor relations template library gives teams a starting point for turning investor communication and onboarding steps into structured workflows.

Operational due diligence readiness

Operational due diligence is not a one-time scramble before an allocator review. It is the ongoing ability to show how the fund governs people, systems, controls, service providers, cybersecurity, valuation, compliance, and business continuity. A fund that runs controlled processes every week has a much easier time responding to diligence requests.

A dedicated operational due diligence checklist for hedge funds can help standardize evidence collection before investor or consultant reviews.

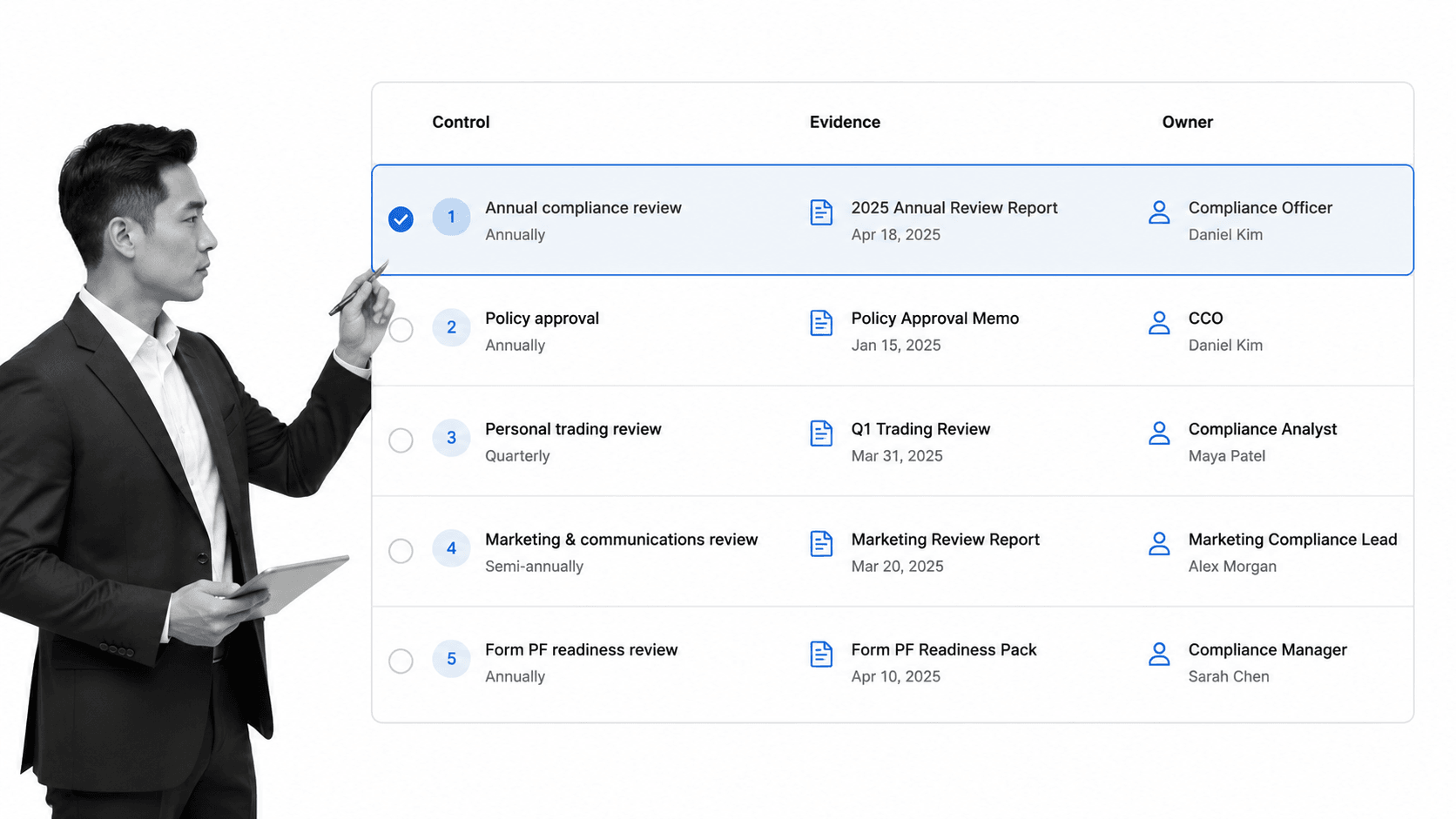

Hedge fund compliance processes

Hedge fund compliance processes translate regulatory obligations and internal policies into recurring work. The fund may rely on outside counsel, compliance consultants, administrators, and technology providers, but internal ownership still matters. Someone has to confirm the work happened, exceptions were handled, and records are retained.

Common compliance processes include:

- Annual compliance program review.

- Policy approval and version control.

- Employee personal trading reviews.

- Code of ethics certifications.

- Marketing material review.

- Restricted list and watch list checks.

- Outside business activity and gifts review.

- Regulatory filing preparation and signoff.

- Cybersecurity and vendor risk review.

- SEC exam readiness and document request response.

Form PF is a useful example of why process matters. The SEC’s form structure includes sections for all filers, private funds, and hedge funds. The Office of Financial Research notes that SEC-registered investment advisers with at least $150 million in private fund assets under management are required to file Form PF. Whether a particular adviser must file, and what it must complete, depends on the adviser’s registration status, assets, fund types, and other facts. That creates a process requirement: determine applicability, collect data, validate it, review it, file it, and retain evidence.

The same logic applies to Form ADV, annual reviews, and internal compliance certifications. A page like Form ADV can explain the filing context, but the operating question is whether the firm has a recurring workflow that makes the filing dependable.

Compliance processes need evidence by design

A compliance process should not rely on someone remembering to save an email thread. Evidence should be required as part of the workflow. Examples include signed certifications, reviewed reports, screenshots, policy versions, approval records, exception notes, and remediation tasks.

Compliance onboarding is a process too

New compliance analysts need firm context, regulatory context, tools training, escalation rules, and policy orientation. A hedge fund compliance analyst onboarding workflow helps make that ramp consistent.

Hedge fund risk and control processes

Risk processes make risk visible, but control processes make risk actionable. A risk report that nobody reviews is not a control. A control is a defined activity with an owner, cadence, evidence, escalation path, and review standard.

For hedge funds, risk and control processes often cover:

- Investment limits: exposure, concentration, leverage, liquidity, and mandate constraints.

- Valuation controls: pricing source review, fair value support, stale price checks, and approval of overrides.

- Counterparty controls: onboarding, credit review, exposure monitoring, and documentation.

- Operational controls: reconciliations, access reviews, change management, incident response, and business continuity.

- Compliance controls: employee certifications, restricted list checks, marketing review, and books and records retention.

A mature operational risk management framework helps connect those controls to actual work. The practical goal is simple: every important risk has an owner, every control has a cadence, and every exception has a path to closure.

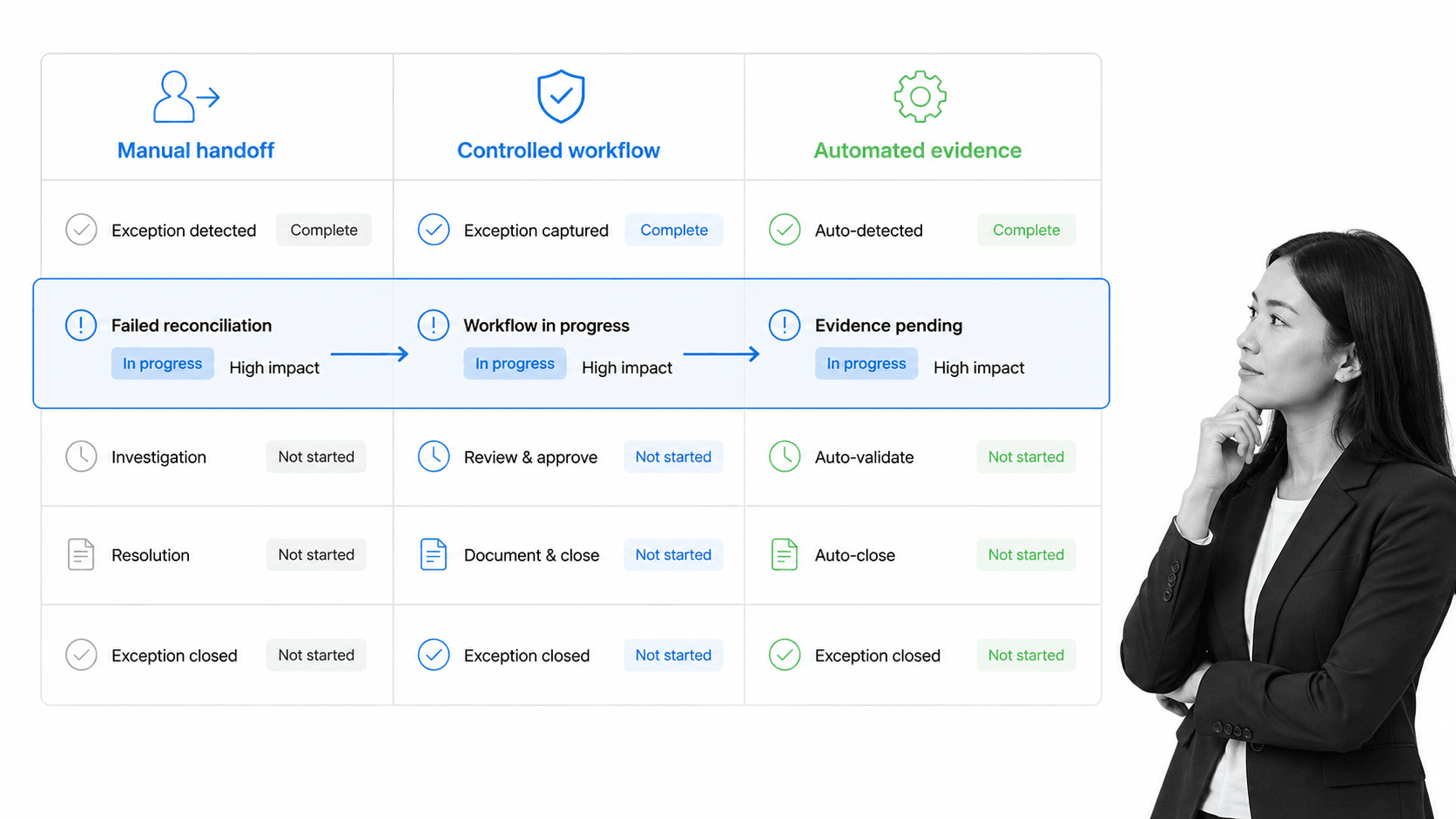

Exception management is the control center

Exceptions are where process quality becomes visible. A failed reconciliation, missing approval, pricing question, late filing input, or unresolved investor document should not sit in a personal inbox. It should trigger a workflow with severity, owner, due date, evidence, escalation, and final review.

Control reviews should feed improvement

The point of a control review is not just to pass the review. It should expose where the process needs redesign. If the same exception appears every month, the issue may be unclear ownership, weak system integration, bad source data, or an approval step that happens too late.

How to document hedge fund processes

Good documentation turns hedge fund processes into usable operating assets. It should be specific enough for a new owner to run the process, structured enough for compliance to review, and current enough that teams trust it.

Each process should answer these questions:

- Purpose: what risk, obligation, or operational outcome does this process control?

- Trigger: what starts it: a trade, new investor, calendar date, filing deadline, exception, or request?

- Owner: who owns the process end to end?

- Inputs: what data, documents, approvals, or system records are required?

- Steps: what happens, in what order, with what decision points?

- Controls: which steps require review, approval, evidence, or segregation of duties?

- Exceptions: what can go wrong, how is it escalated, and who closes it?

- Evidence: what proof is retained and where?

- Review cadence: how often is the process tested or improved?

Teams often start with a policy document, then build the workflow underneath it. That works if the document and workflow stay connected. It fails when the document says one thing and the team does another.

Process documentation should also avoid false precision. You do not need a 40-page SOP for every routine. You need enough structure that the process can be run, reviewed, and improved without relying on the same person being available every time.

Use tiers for process criticality

Not every process needs the same control depth. A marketing request and a Form PF data collection workflow should not have the same evidence standard. Industry operating guides, including the AIMA and Bloomberg hedge fund startup guide, separate legal, tax, technology, service provider, trading, and operational decisions because each area carries different process risk. Tier processes by risk: critical regulatory, investor-facing, financial close, investment control, operational support, and administrative.

Map systems of record

Every documented process should name the systems involved. That may include order management, portfolio accounting, CRM, document storage, email, administrator portals, data rooms, reporting tools, and workflow software. If a handoff crosses systems, document the handoff.

How to improve hedge fund processes with automation

Automation improves hedge fund processes when it reduces variance, enforces controls, and captures proof. It is not just about moving faster. It is about making the right way the default way.

A practical improvement sequence looks like this:

- Inventory recurring processes. Start with monthly close, compliance calendar, investor requests, onboarding, reconciliations, risk reviews, and due diligence evidence.

- Rank them by risk. Prioritize processes that affect investors, filings, financial statements, controls, or exam readiness.

- Define the trigger and owner. Every recurring workflow needs a clear start condition and accountable owner.

- Convert the SOP into a workflow. Turn static instructions into assigned tasks, conditional paths, required fields, and approvals.

- Make evidence mandatory. Require uploads, links, confirmations, or structured fields at the step where the evidence is created.

- Add escalation rules. Late tasks, failed reconciliations, missing approvals, and unresolved exceptions should trigger follow-up automatically.

- Review process data. Use cycle time, exception rates, overdue tasks, and recurring bottlenecks to improve the process.

Process Street has direct, universal integrations to 5,000+ systems. Need a new one? An AI agent builds it on the fly. That matters for hedge fund operations because the process often spans systems: CRM, data room, accounting platform, administrator portal, document repository, and communication tools.

For teams comparing the broader software landscape, hedge fund tools and hedge fund software can help separate point solutions from systems that actually enforce recurring work.

Start with the highest-friction handoffs

The best first automation target is rarely the most complex process. Start where handoffs are frequent, mistakes are visible, and evidence is painful to collect. Trade break resolution, compliance certifications, due diligence evidence collection, and monthly close review are common starting points.

Keep humans in the approval loop

Automation should not erase judgment. Hedge fund work often requires review by investment, operations, finance, legal, or compliance owners. A good workflow automates routing, reminders, evidence collection, and escalation while preserving the human approval where judgment matters.

Hedge fund process checklist

Use this checklist to audit whether a hedge fund process is strong enough to run without constant heroics:

- The process has one accountable owner.

- The trigger is clear and repeatable.

- Every task has an owner, due date, and completion standard.

- Approvals happen inside the workflow, not only in email.

- Required evidence is captured at the step where work occurs.

- Exceptions have severity, owner, due date, and closure criteria.

- The workflow references the current policy or SOP version.

- Service provider handoffs are visible.

- Regulatory and investor-facing deadlines are built into the calendar.

- The process is reviewed after recurring exceptions or material changes.

If you are starting from scratch, build from the workflows that already matter. Hedge fund checklists, hedge fund operational due diligence, hedge fund risk management, and hedge fund due diligence are natural process families to standardize first.

For fund launch and adjacent private capital work, a venture capital fund formation checklist can also help teams think through formation, investor, and role assignment steps in a structured way.

Hedge fund processes FAQs

What are hedge fund processes?

Hedge fund processes are the recurring workflows a fund uses to manage investment research, trading, risk, compliance, fund accounting, investor communication, and operational controls. They define owners, steps, approvals, evidence, and exception paths so work happens consistently.

What are the most important hedge fund operations processes?

The most important hedge fund operations processes usually include trade capture, allocation, reconciliation, NAV support, investor onboarding, investor reporting, compliance reviews, risk monitoring, and exception management. The exact priority depends on fund strategy, asset class, investor base, and regulatory profile.

How do hedge funds document compliance processes?

Hedge funds document compliance processes by linking policies to recurring workflows, assigning owners, defining required evidence, recording approvals, and retaining proof of completion. The documentation should show what must happen, who does it, when it happens, and how exceptions are resolved.

How can hedge funds improve operational controls?

Hedge funds can improve operational controls by standardizing recurring workflows, requiring evidence at the task level, adding approval gates, escalating overdue or failed steps, and reviewing exception trends. Controls work best when they are built into daily execution rather than checked after the fact.

What is the difference between front office, middle office, and back office hedge fund processes?

Front office processes cover investment research, portfolio decisions, and trading. Middle office processes cover trade capture, risk monitoring, allocation, reconciliation, and exception handling. Back office processes cover accounting, NAV support, investor reporting, compliance records, audit support, and service provider coordination.

Which hedge fund processes should be automated first?

Automate the processes with the highest combination of recurrence, risk, handoffs, and evidence burden first. Common starting points include compliance calendars, monthly close review, trade break resolution, investor document collection, operational due diligence evidence, and recurring certifications.