The world is full of ideas, especially in the business world, where rapidly growing competition has made innovation mandatory. Your idea can be a real game-changer, but that does not mean anything if you do not know how to set it in motion in the right way. If you own a startup, you probably cannot wait to see it launch, and that is completely natural.

Startup law is less about paperwork for its own sake and more about precision. Think of those space movies with close-ups of faces behind monitors drenched in sweat: if you are off by even a small legal degree at launch, the deviation is multiplied as you hire, raise money, sign customers, and build intellectual property. The legal mistakes startups make can turn big dreams into nightmares, but the law can also be a useful tool on the road to success when you learn to recognize its traps and turn them into advantages.

The following is a guest post from Nick Brown. Nick is a blogger and marketing expert who has worked on business and marketing resources for early-stage companies.

This article is general information, not legal advice. Startup law changes by jurisdiction, business model, funding plan, and ownership structure. Use it as a checklist for what to discuss with qualified counsel, not as a substitute for counsel.

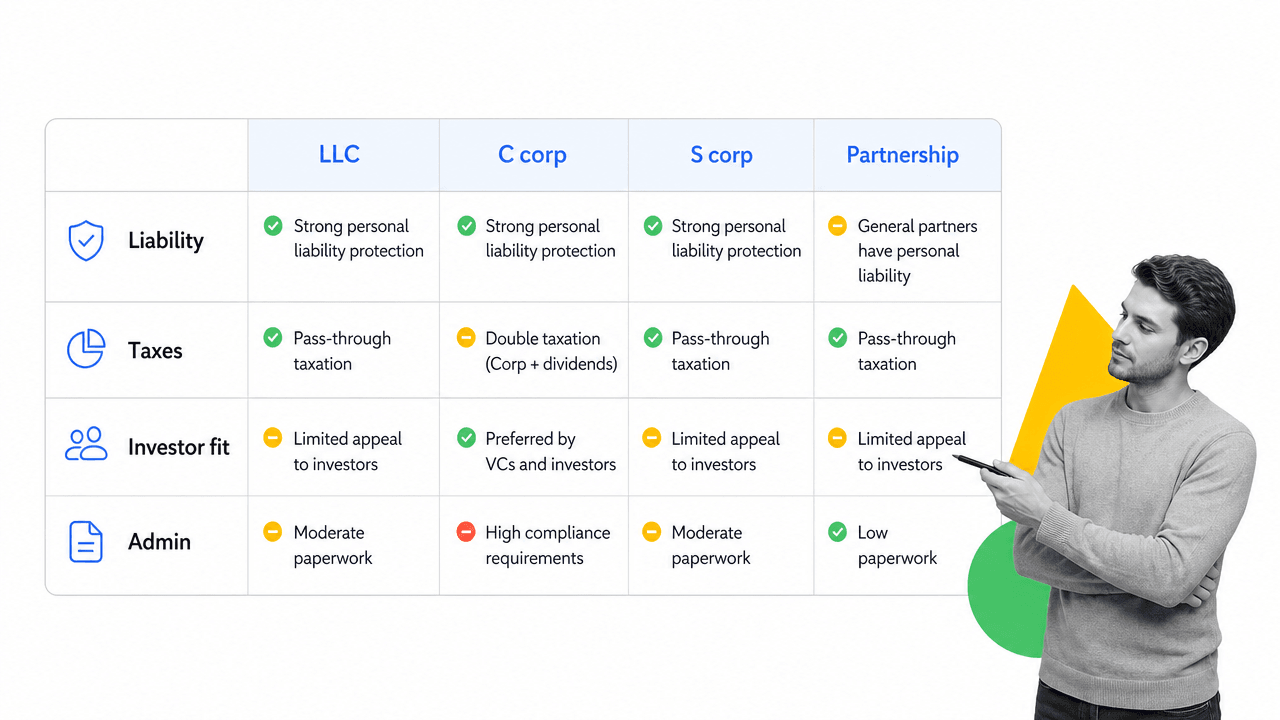

1. Not knowing an LLC from a C-corp

Before you can interpret and pursue your dream, you need to give it a concrete form. That is why one of your first business decisions as a founder is to choose the right legal structure in which you will operate. The wrong structure can create avoidable tax, liability, governance, and fundraising problems. The IRS business-structures guide still frames the basic choices as sole proprietorship, partnership, corporation, S corporation, and LLC, but the right answer depends on what you are building.

A sole proprietorship is simple, often requiring fewer filings, fees, or legal documentation beyond local business and state permits. The disadvantages are serious: there is only one owner, which limits how another investor can put in capital, and there is no liability wall between personal assets and business obligations. A general partnership can work for a small service business, and partners can set the rules together through a partnership agreement, but each partner can expose personal assets to business debts if creditors sue. Those structures can be useful in narrow cases, but they are usually a poor default for a startup that expects outside capital, employees, regulated data, or material contract risk.

LLCs are formed under state law and can work well for closely held companies, pass-through tax planning, agencies, holding companies, or founders who do not expect venture financing. They can also create friction later if the company needs to convert for investors, equity incentives, or complex cap-table work.

C corporations are also formed under state law and remain the standard path for many venture capital-backed companies because investors, equity plans, and future financing rounds are built around corporate stock. S corporations can offer favorable tax treatment, but they come with eligibility constraints. IRS material still describes S corporations as limited to no more than 100 shareholders and other ownership restrictions. A limited partnership, often used for hedge funds, private equity firms, or investment real estate, is another state-law option, but it is rarely the obvious default for an operating startup.

The practical move is simple: decide based on your funding plan, tax profile, ownership model, accounting requirements, and state law before you start signing contracts. LLCs, corporations, and limited partnerships usually have higher costs of forming and operating than sole proprietorships and partnerships because of accounting, legal, and tax issues, but they can also offer liability protection from creditors, greater ease in raising capital, and potential tax advantages. You can later convert partnerships and sole proprietorships to an LLC, S corporation, C corporation, or another legal entity, but conversions can have significant costs. The SBA business-structure guide is a useful primer, but a startup attorney and tax adviser should help you choose before the choice becomes expensive to unwind.

2. Not making crystal clear agreements with your co-founders

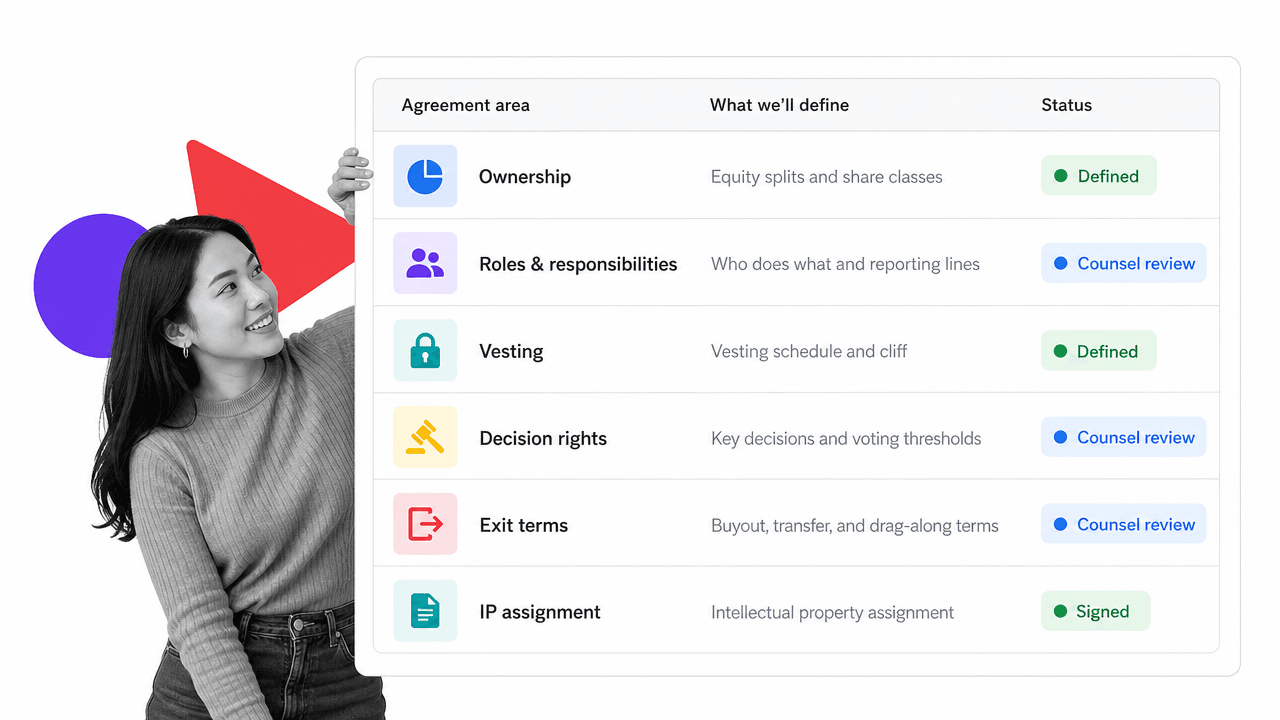

Nobody is able to start a business completely alone. In order to make a dream come true, you need to assemble other people who share it. Even when co-founders come together around one dream, that does not mean each person has the same picture in their head, or the same assumptions about control, ownership, effort, compensation, and what happens if someone leaves.

The questions will rise eventually: who owns what, who controls what, who does what, how equity vests, how disputes are handled, and what happens if a founder stops contributing. It is better to pose them at the beginning, because they define every co-founder’s responsibilities and reduce the possibility of future dispute. If those answers are not written down while the company is still low-value and relationships are still good, the later version is harder, more emotional, and usually more expensive.

This matters even in a 50/50 partnership. Equal ownership sounds fair at the start, but deadlocks, unclear roles, and uneven contributions can make it fragile. Everybody is in it together, but roles still need to be clearly defined. Founder agreements should cover voting, board or manager control, equity vesting, intellectual property assignment, confidentiality, termination, buyback rights, and dispute resolution.

Timing also matters. Waiting to issue or document founder equity can create tax consequences, including phantom income risk. Founders should talk to counsel and a tax adviser about equity grants, vesting, fair market value, and any election deadlines before the company value starts moving. Guides like Stripe Atlas on startup equity are helpful for orientation, but the actual paperwork should match your company.

3. Leaving rules unwritten (and non-existent)

All dreamers are enthusiasts, and early teams often move fast because everyone knows everyone. That is useful until the company starts relying on memory, old email threads, correspondence, and informal promises as its operating system. There is nothing wrong with starting with friends, family, partners, or co-founders, as long as the required documentation does not become sloppy.

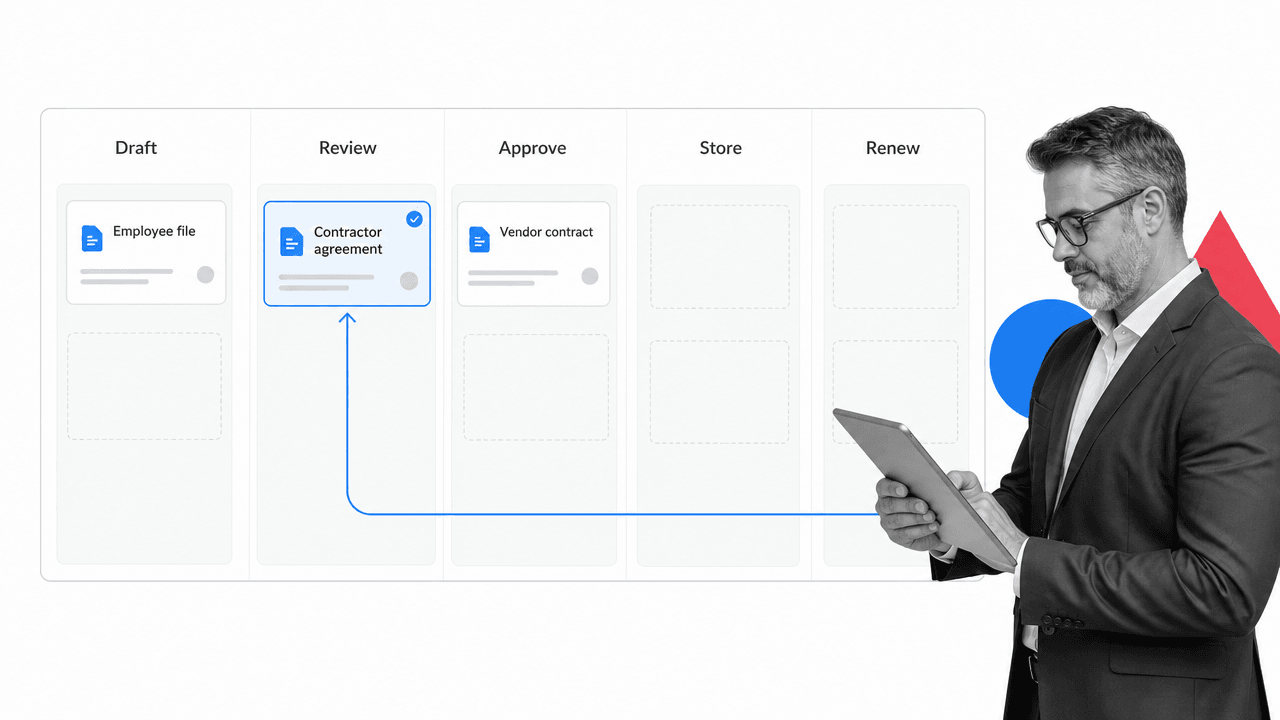

Founder titles, responsibilities, and duties; employee files; contractor agreements; customer terms; vendor contracts; privacy obligations; IP assignments; and approval records all need a place to live. If a founder, employee, contractor, uninvolved party, or early adviser later appears claiming they were promised a certain share, equity, or ownership in the product, written agreements and clean records can be the difference between a manageable dispute and a financing-killing mess. The simple mistake of not putting it on paper can cost you a lot, including derailing potential investments.

This is where legal operations and company operations overlap. The point is not to create a graveyard of PDFs. The point is to turn important legal obligations into repeatable workflows: draft, review, approve, sign, store, renew, and audit. A legal document management software system helps keep legal records findable, but the stronger pattern is to connect records to the workflow that proves they were reviewed and followed.

Process Street is a Compliance Operations Platform that brings Docs, Ops, and Cora together so teams can document policies, execute the work tied to those policies, and monitor whether the process is being followed. For startups, that means founder agreements, employment documentation, vendor reviews, customer contract steps, and renewal reminders can live in one governed operating system instead of scattered across inboxes and drives.

Templates can help, but they are not a substitute for judgment. Use contract templates to standardize recurring work, then route exceptions to counsel. Although people refer to standard form contracts, there is nothing truly standard about them: they can be tailored to be more favorable to a particular side, and an experienced business lawyer should review drafting that could create liability claims or disputes. If you use automations, make sure the workflow still produces evidence: who reviewed the agreement, which version was approved, who signed, where it was stored, and when it should be revisited. Process Street also supports integrations through tools such as Zapier, so routine legal operations can connect to the rest of your stack without manual chasing.

4. Choosing a ‘single-purpose’ lawyer

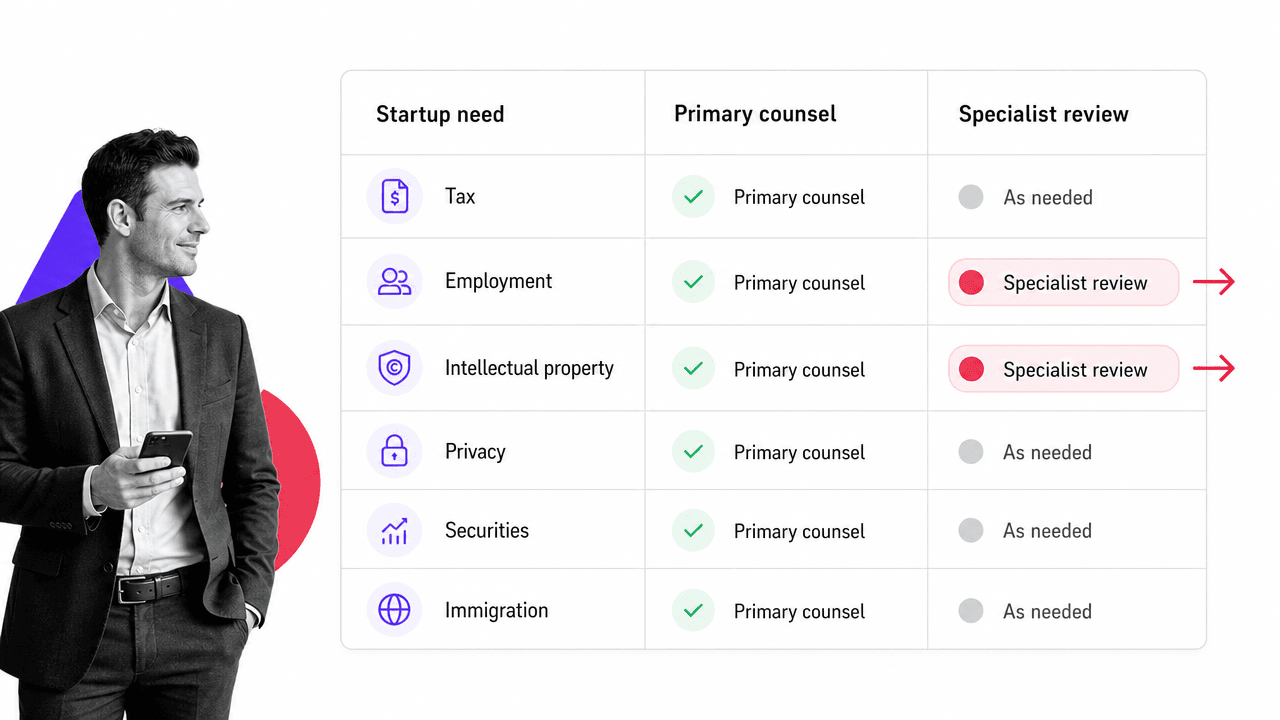

A family member who happens to be a lawyer may be useful in one area, but startups rarely have one legal problem. It is okay to try to save on expenses, but that effort can easily be misguided if one field is treated as enough. Formation, tax, employment, IP, privacy, securities, franchise, immigration, commercial contracts, and real estate can all appear earlier than founders expect.

You do not need a full bench of specialists on day one. You do need a primary business attorney who understands startups well enough to know when a specialist is required. In order to acquire experienced legal advice across every field, founders sometimes combine several law firms or lawyers with different areas of expertise. A general startup lawyer can coordinate the formation plan, founder paperwork, customer contracts, and basic employment documents, while preserving continuity in communication with your legal counsel. Specialists should come in when the risk is too specific to treat casually.

Common specialist triggers include issuing equity, raising money, hiring across state or country lines, using contractors for core product work, handling regulated customer data, filing patents, registering trademarks, entering a franchise model, signing a lease, or selling into a regulated industry. Some young businesses decide to go international and need immigration advice before a road trip, investor meeting, or business partner conversation creates avoidable trouble. The same is true with intellectual property rights, whether you are planning to gain a trademark license, respond when copyrighted work is reproduced, or draft a patent application.

The mistake is not trying to control legal spend. The mistake is treating legal coverage as one flat category. Pay for the right review at the moment when the decision is still cheap to change. That is usually less expensive than asking a lawyer to repair the wrong entity, a bad contractor agreement, a broken privacy promise, or IP ownership that was never assigned to the company.

5. Getting your idea stolen before it materializes

As soon as you tell your dream to other people, it becomes open to different interpretations. Sometimes a listener will make sense of it quicker than the person who actually dreamt it. The same goes for business ideas that need time to develop and blossom: they become vulnerable as soon as they leave your head. Sometimes that risk comes from outsiders. More often, it comes from unclear ownership inside the company: founders, employees, contractors, advisers, agencies, or early collaborators who helped create the product but never assigned rights to the company.

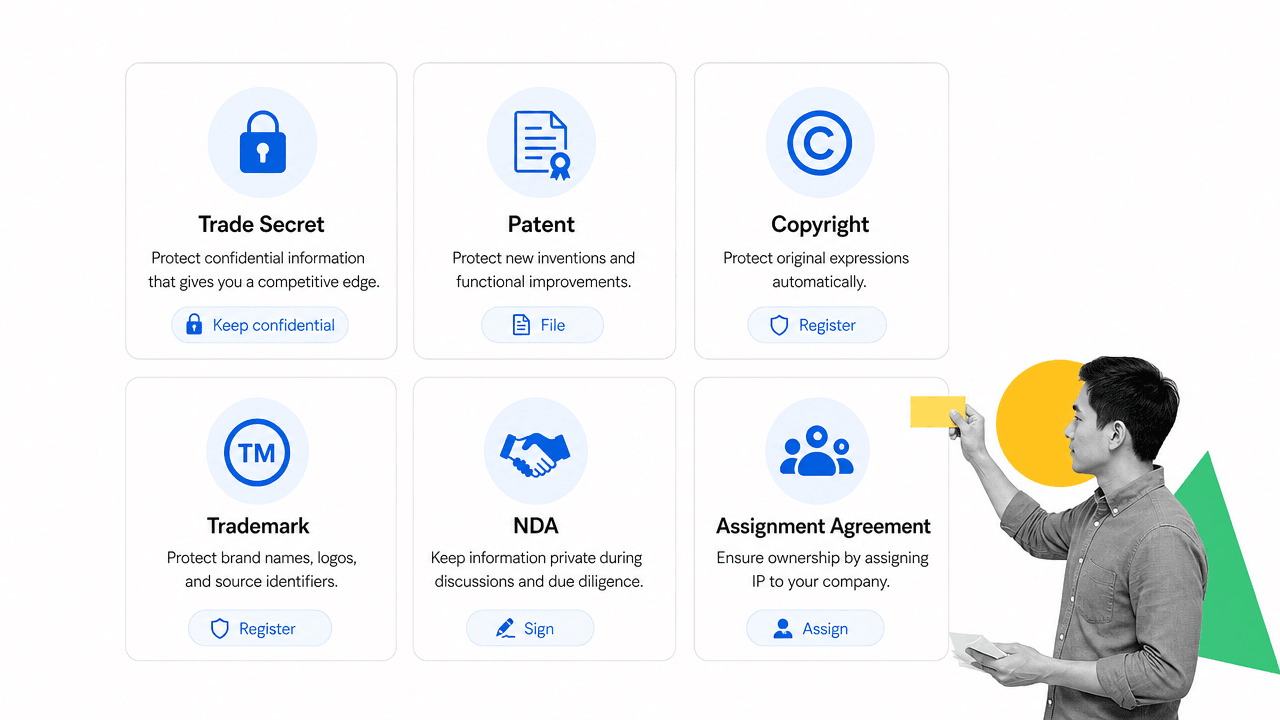

Treat intellectual property as a set of tools, not a single magic filing. Before you develop a concrete shape of the idea or obtain a patent, a trade secret can protect information that stays confidential. NDAs and confidentiality clauses help preserve that confidentiality during discussions and reduce the chance that information will leak from the inside. IP assignment agreements help make sure work created for the company is owned by the company. Orrick has a useful explainer on why companies should secure IP created by employees, consultants, and others.

Patents can protect certain new and useful inventions, but they are expensive, slow, and not always the right tool. A patent generally requires a concrete embodiment, originality, novelty, no prior patent or printed publication that already describes the invention, and a useful purpose. The patent’s claims define the protected invention, and the process can take years, so an experienced patent lawyer should draw up the patent application when a patent is the right route. The USPTO patent process overview is a better starting point than assuming every product idea should become a patent application.

Copyright protects original works such as software code, books, music, articles, movies, advertising copy, video, artwork, and similar expression. Copyright can give an owner exclusive rights to make copies and produce derivative works such as revisions or sequels. The U.S. Copyright Office FAQ explains the basics. Copyright does not protect a business idea itself, so do not rely on it to solve ownership issues that should have been handled through assignment agreements.

Trademarks protect brand identifiers such as names, symbols, and words used to distinguish goods or services from those of others. Think of the symbolic value behind marks such as American Express or Coca-Cola. You can build some rights by using a mark in commerce, but federal registration has meaningful advantages. The USPTO explains that registration can create nationwide rights, public notice, and a legal presumption of ownership. Use the USPTO trademark registration guide before assuming your brand is protected because you bought a domain name.

The legal side of business can feel like a thick, dark forest in the center of your dreamland. The safest operating habit is to keep your path structured: map what your startup is creating, who is creating it, what protection strategy applies, what document proves ownership, and which advisers belong along the way. That map should be part of your startup legal checklist before fundraising, hiring, or enterprise sales due diligence begins.

FAQs

Do startups need a lawyer before launching?

Most startups should speak with a qualified lawyer before formation, founder equity, hiring, fundraising, or customer contracts. You may not need a large legal budget on day one, but you do need the right structure and ownership documents before mistakes compound.

Should a startup choose an LLC or a C corporation?

It depends on the funding plan, tax profile, ownership structure, and state law. LLCs can fit closely held or pass-through businesses. C corporations are common for venture-backed startups because investors, stock plans, and financing rounds usually expect that structure.

How can founders protect startup IP early?

Start with confidentiality, invention assignment, contractor IP assignment, founder IP assignment, and clean records of who created what. Then decide whether trade secret protection, copyright, trademark registration, or a patent application fits the specific asset.

What legal documents should every startup track?

Core documents usually include formation records, founder agreements, equity documents, IP assignments, contractor agreements, employee records, customer contracts, vendor agreements, privacy documents, board or consent records, and renewal or filing deadlines. The exact set depends on the company and jurisdiction.

Get started with Process Street to turn legal checklists, approvals, renewals, and compliance tasks into workflows your team can actually follow.