Turn every policy into automated workflows with built-in enforcement and audit-ready proof.

Wealth Management Technology

Wealth management technology is the set of systems, workflows, data connections, and controls that help advisory firms serve clients, manage portfolios, document decisions, and prove compliance.

The category is broader than a single wealth management platform. It includes CRM, client portals, financial planning tools, portfolio reporting, document collection, risk profiling, approval workflows, integrations, analytics, and the compliance evidence that sits behind client work.

This guide explains what belongs in the stack, why it matters now, how to implement it without creating tool sprawl, and where workflow automation fits for advisor, operations, and compliance teams.

In this article, we are going to cover:

- What wealth management technology means

- Why wealth management technology matters now

- Core components of wealth management technology

- How to implement wealth management technology

- Wealth management technology and compliance

- Wealth management technology in Process Street

- How to evaluate wealth management technology

- FAQs

What wealth management technology means

Wealth management technology gives advisory firms an operating layer for client service. At its best, it turns a set of disconnected tasks into a governed client journey: prospect intake, discovery, risk review, planning, account opening, investment policy, portfolio monitoring, service requests, review meetings, and ongoing documentation.

The word technology can make the discipline sound like an IT project. In practice, the work is operational. Advisors need cleaner handoffs. Operations teams need fewer manual checks. Compliance teams need evidence. Clients expect digital convenience without losing human advice.

It connects the advisor experience

Advisors do not need another login that adds admin work. They need a connected workspace where client context, next steps, forms, approvals, notes, and portfolio updates stay synchronized.

That is why a broad wealth management platform strategy usually matters more than one feature. The goal is not to buy a shiny portal. The goal is to reduce friction across the whole advice lifecycle.

It connects the client experience

Clients feel technology through small moments. They notice whether forms are easy to complete, whether requests are repeated, whether meetings start with the right context, and whether the firm follows through quickly after advice is given.

A wealth technology stack should make those moments consistent. If a client uploads a trust document, the workflow should route it to the right owner, update the checklist, trigger the next task, and preserve evidence for later review.

It connects the control environment

Wealth management is a trust business. The technology stack has to support suitability, privacy, cybersecurity, documentation, supervision, and approval requirements without forcing every control into email.

Controls work best when they sit inside the workflow. A risk review, investment policy update, Form ADV delivery, exception approval, or account opening check should produce proof as the work happens.

That control environment also needs clear ownership. If client data is wrong, someone has to correct it. If a document is missing, someone has to chase it. If an exception is approved, someone has to record why. Wealth management technology should make those ownership lines visible instead of leaving them buried in inboxes.

Why wealth management technology matters now

Wealth management technology matters now because firms are being squeezed from several directions at once: client expectations are rising, advisor capacity is limited, compliance expectations keep changing, and AI is entering the operating model.

A recent Deloitte wealth management technology study describes technology as a source of competitive advantage, especially for advisor enablement, automation, AI adoption, and platform modernization.

Advisor capacity is the constraint

The expensive part of the operating model is not only software. It is advisor and operations time. Every manual data entry, missing document chase, untracked approval, and unclear next step steals capacity from client work.

Good wealth management technology removes low-value work from the advisor day. It does not replace advice. It protects the time advisors need for planning, relationship management, and judgment.

Client expectations are digital by default

Deloitte digital wealth manager perspective frames the industry goal around a digitally enabled, personalized, scalable model. That is difficult when client data, tasks, and documents live across disconnected tools.

The client does not care which system owns the handoff. They care whether the firm knows who they are, responds quickly, and avoids asking for the same information twice.

AI raises the control bar

AI can summarize meetings, draft follow-up, classify documents, suggest next steps, and monitor workflows. But wealth firms cannot treat AI as a loose assistant sitting outside the control environment.

If AI supports advice operations, exception detection, or workflow routing, firms need a governance lens. The NIST AI Risk Management Framework is a practical reference for thinking about measurement, oversight, and risk.

The practical question is not whether AI can speed up a task. It is whether the firm can show what the AI touched, what a human reviewed, and which control decided the next step. That is why workflows, approvals, and audit history become more important as automation gets stronger.

Core components of wealth management technology

A wealth management technology stack needs to support the full lifecycle of advice, not just the front-office moments clients see. The components below are the practical building blocks.

Client relationship management

The CRM is usually the relationship spine. It stores client households, contacts, opportunities, service history, activity notes, meeting follow-up, and advisor ownership. But the CRM should not become the only process tool.

When every workflow is forced into CRM fields, the firm often loses task-level control. A better pattern is to keep the CRM as the client record and connect it to workflow systems that run repeatable work.

Client onboarding and document collection

Onboarding is where many firms feel the pain first. The workflow crosses discovery, KYC, suitability, account opening, document collection, fee setup, investment policy, and approvals. A structured client onboarding for financial services template can help turn that work into a repeatable process.

Broader guidance on client onboarding and the customer onboarding process shows why the handoff matters before the client relationship becomes complex.

Planning, portfolio, and reporting systems

Financial planning, portfolio accounting, performance reporting, billing, rebalancing, and investment analytics tools support the technical side of advice. These systems need clean data and clear review points.

Broadridge wealth management platform guide describes a wealth management platform as an integrated system for client service, operations, and compliance. That integration is what turns reporting into action.

Workflow, compliance, and evidence

Workflow technology makes the process enforceable. It decides who does what, which evidence is required, when an approval is needed, and how exceptions are recorded.

Adjacent pages on financial compliance software, compliance management software, and compliance as proof of control explain the evidence side of controlled execution.

This layer is often the difference between a technology stack and an operating system. A stack can hold useful tools, but an operating system tells the firm what happens next. It keeps the client journey moving while protecting the controls that make the work defensible.

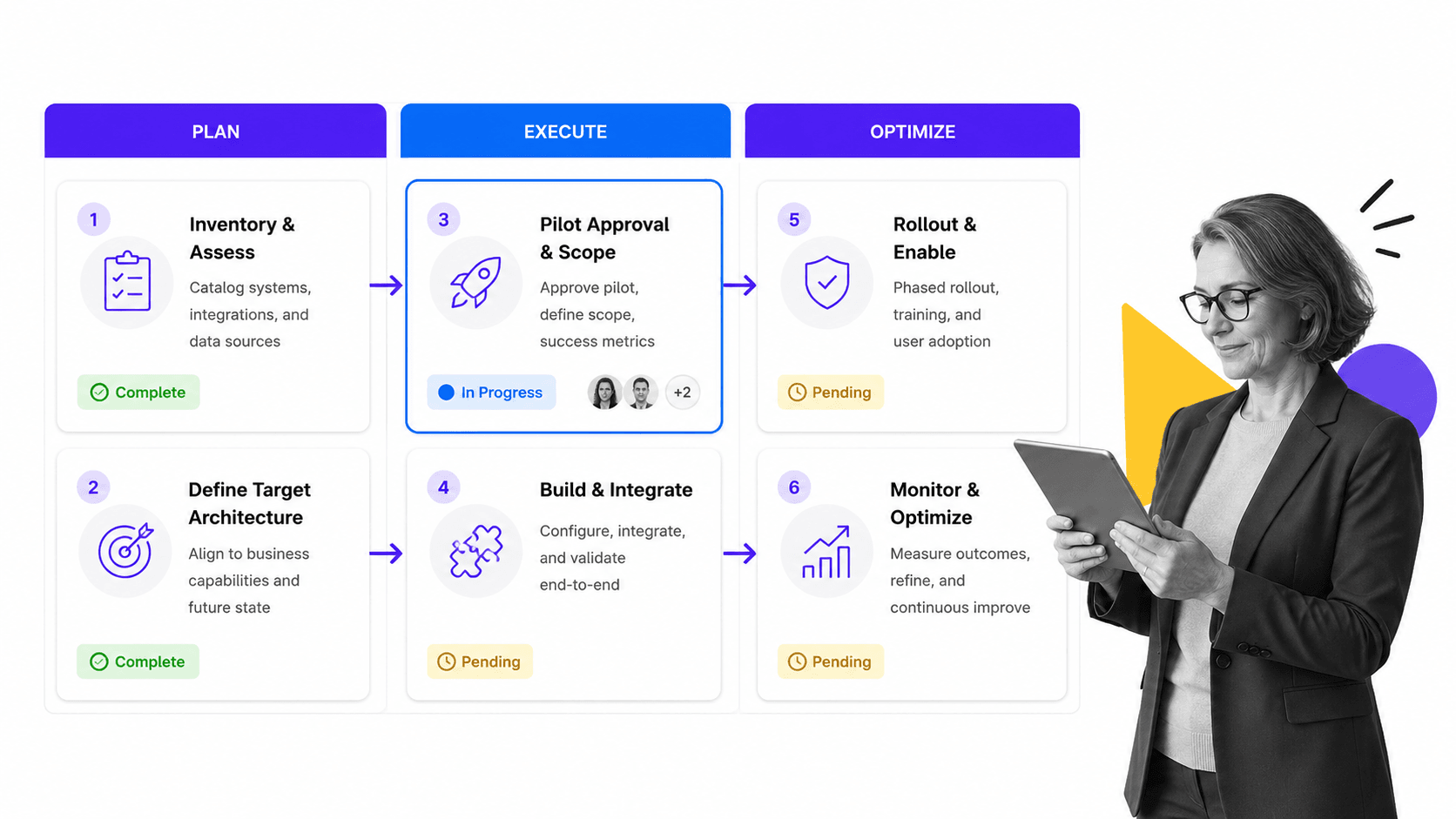

How to implement wealth management technology

Implementing wealth management technology is not a procurement exercise. It is an operating-model change. The safest approach is to start from workflows, then map the systems that support them.

Step 1: Inventory the client journey

List the major client journeys: prospect intake, new client onboarding, account transfer, review meeting prep, portfolio change request, beneficiary change, document update, exception review, and annual compliance tasks.

For each journey, record the owner, systems touched, required evidence, approval points, client-facing steps, and failure modes. This prevents the firm from buying software for a symptom instead of fixing the workflow.

Step 2: Identify the system of record and system of action

A system of record stores the authoritative data. A system of action runs the work. Confusing the two creates clutter. Your CRM, portfolio system, and document repository may store records, while a workflow platform coordinates the tasks and approvals around those records.

Step 3: Pilot one high-friction workflow

Pick one workflow with clear pain and measurable improvement. Client onboarding, review meeting prep, RIA compliance review, account maintenance, and document collection are common starting points.

Workflow capabilities like approvals, conditional logic, and run links help route work without asking people to remember every branch.

Step 4: Build controls into the workflow

Do not bolt controls on after launch. Define evidence fields, approval thresholds, exception routes, retention needs, and audit checks while the workflow is being designed.

Step 5: Optimize from execution data

Once the workflow is live, review where tasks stall, where evidence is missing, which approvals are repeated, and which exceptions keep appearing. That data should feed process improvement.

Teams looking at adjacent automation patterns can compare financial process automation, financial process management, and a broader workflow management system.

Treat rollout as a controlled release, not a single launch event. Document what changed, train the roles affected, monitor completion quality, and keep an exception path open for cases the new workflow does not yet handle. That prevents the firm from replacing old manual chaos with new digital confusion.

Wealth management technology and compliance

Compliance is not a side module in wealth management technology. It is part of the operating model. Firms need to prove that client work followed the right process, not only that a form exists somewhere.

Registration and disclosure workflows

Investment advisers operate in a documented regulatory environment. SEC materials on SEC investment adviser registration information and related disclosure obligations show why process evidence matters.

A page on Form ADV covers one of the core disclosure documents. The same principle applies across the broader stack: document the requirement, run the workflow, and keep proof.

Cybersecurity and data handling

Wealth firms manage sensitive personal and financial information. SEC guidance on SEC investment adviser cybersecurity guidance reinforces the need for controls around information handling, incident response, and operational resilience.

Technology choices should make those controls easier to execute. Access reviews, vendor checks, evidence collection, approval routing, and exception tracking should be routine, not a scramble.

Supervision and exception management

The stack should make exceptions visible. If a client file is missing evidence, an account update needs review, or a risk profile is stale, the system should route the issue to the right owner and preserve the action taken.

That is where operational risk management framework thinking becomes useful. Operational risk drops when controls are attached to the work instead of hidden in policy documents.

Exception handling should be designed before it is needed. Define which exceptions can be resolved by an advisor, which need operations review, which need compliance approval, and which must be escalated. The workflow should make that path obvious in the moment, not after a supervisor asks for proof.

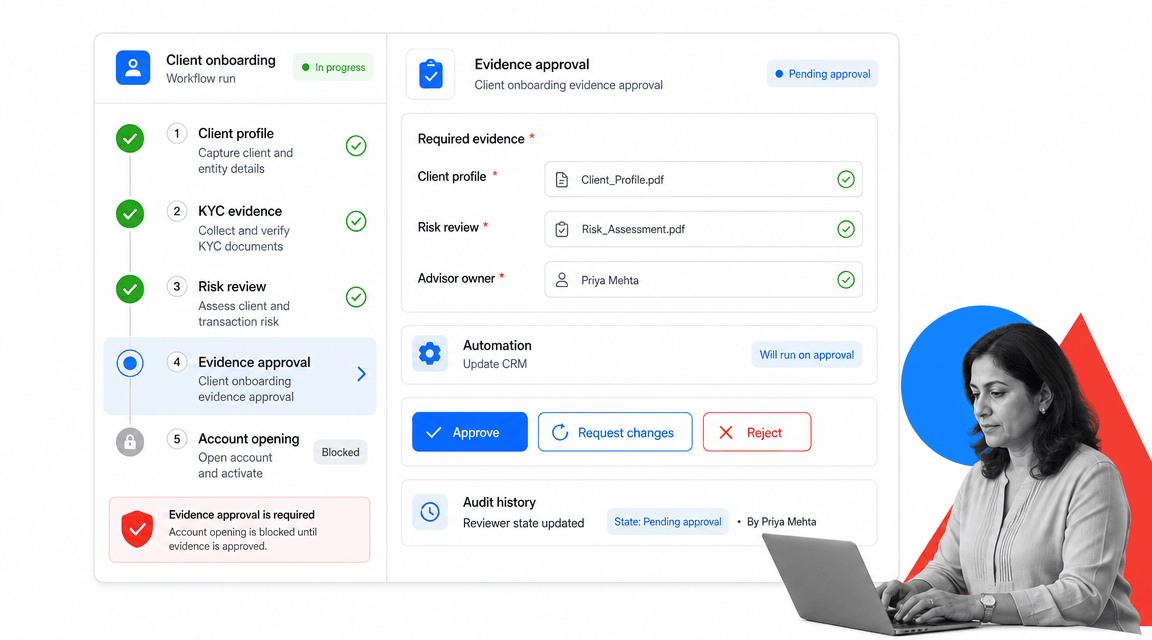

Wealth management technology in Process Street

Process Street supports wealth management technology by turning client, advisor, operations, and compliance procedures into controlled workflows.

Instead of asking teams to remember the process, Process Street makes the process the place where work happens. Required fields collect client context and evidence. Conditional logic routes tasks based on risk, account type, or approval threshold. Approvals hold the workflow until a reviewer signs off.

Run client and advisor workflows

Firms can build workflows for client onboarding, annual review prep, document collection, beneficiary updates, investment policy reviews, vendor checks, complaint intake, cybersecurity review, and compliance attestations.

The general client onboarding process template is a useful example of how repeatable client work can be structured before it is customized to a specific wealth firm.

Keep evidence with the task

The approval record, uploaded documents, field values, comments, and task history stay attached to the workflow run. That helps advisors, operations teams, and compliance teams inspect the same process record.

Connect systems without losing control

Process Street has direct, universal integrations to 5,000+ systems. Need a new one? An AI agent builds it on the fly. That lets a wealth firm coordinate work across CRM, portfolio, document, communication, and reporting systems while keeping the workflow as the control surface.

Firms that need a deeper comparison of workflow software can use the workflow management software guide as a category reference.

The practical value is simple: the firm can run the client process, not just describe it. Each owner sees the next step, the workflow collects the required evidence, and the system preserves proof for later review.

How to evaluate wealth management technology

Evaluate wealth management technology by asking whether it improves execution, advisor capacity, client experience, and control quality. Feature checklists are useful, but they can hide operating risk.

Does it reduce manual handoffs?

The stack should reduce duplicate data entry, repeated client requests, status chasing, and email-based approvals. If a system adds more admin than it removes, adoption will stall.

Does it preserve clean client context?

Client data should move through the workflow without becoming fragmented. The advisor should understand the current state of the relationship, the next step, and the evidence behind recent decisions.

Does it enforce controls?

Look for required fields, conditional routes, approval gates, exception handling, access controls, audit history, and reporting that shows whether the process was followed.

Can operators own the workflow?

Wealth operations and compliance teams need enough control to adjust workflows as regulations, products, client segments, and internal policies change. IT governance still matters, but every process update should not become a long development cycle.

Does it make AI accountable?

If AI is used to summarize, route, detect exceptions, or generate next steps, the workflow should show what happened, who reviewed it, and which decision was accepted. AI should sit inside a controlled process, not outside it.

Can it support multiple client segments?

A firm may serve emerging affluent clients, high-net-worth households, business owners, retirement plan participants, trusts, foundations, and family offices. The technology stack should adapt the workflow by segment without creating a separate process universe for each group.

That means shared standards with controlled variation. A high-net-worth onboarding workflow may require more entities, documents, approvals, and tax coordination than a simpler household relationship, but the firm should still be able to inspect both through the same operating model.

FAQs

What is wealth management technology?

Wealth management technology is the set of platforms, workflows, data connections, and controls that help advisory firms manage client relationships, portfolio work, documentation, approvals, reporting, and compliance evidence.

Why does wealth management technology matter?

Wealth management technology matters because it helps firms improve advisor productivity, deliver a better client experience, reduce manual handoffs, and prove that regulated client work followed the right process.

What systems belong in a wealth management technology stack?

Common systems include CRM, client portals, planning tools, portfolio reporting, document management, risk profiling, billing, workflow automation, integrations, analytics, cybersecurity controls, and compliance evidence systems.

How should firms implement wealth management technology?

Start by mapping client and advisor workflows, then identify the systems of record and systems of action. Pilot one high-friction workflow, build controls into it, and improve the process using execution data.

How does wealth management technology support compliance?

It supports compliance by embedding required fields, approvals, evidence collection, exception routes, audit history, and review tasks into the work itself. That makes proof easier to produce because the record is created while work happens.

How can Process Street support wealth management technology?

Process Street helps firms run client onboarding, document collection, approval, review, compliance, and operations workflows with required fields, conditional logic, approvals, automations, integrations, and task history.