Bitcoin, Cryptocurrencies, Blockchain.

Bitcoin, Cryptocurrencies, Blockchain.

Together, these various buzzwords form a distributed ledger of hype!

The potential for a new decentralized world has led investors, writers, bankers, entrepreneurs and more to herald various versions and aspects of this new technology as representing the future of humanity.

A World Economic Forum survey even suggested that 10% of global GDP would be stored on the blockchain by 2027.

There is a lot of excitement about the direction the technology is heading, but the tech behind Bitcoin has existed for a while now and we’re yet to see much mainstream integration of it.

Which begs the question: what can the blockchain be used for?

In this Process Street article, we’ll look at:

- What is the blockchain?

- 5 use cases where the blockchain could thrive

- How the blockchain could be utilized in business process management

What is the blockchain? A brief introduction to blockchain

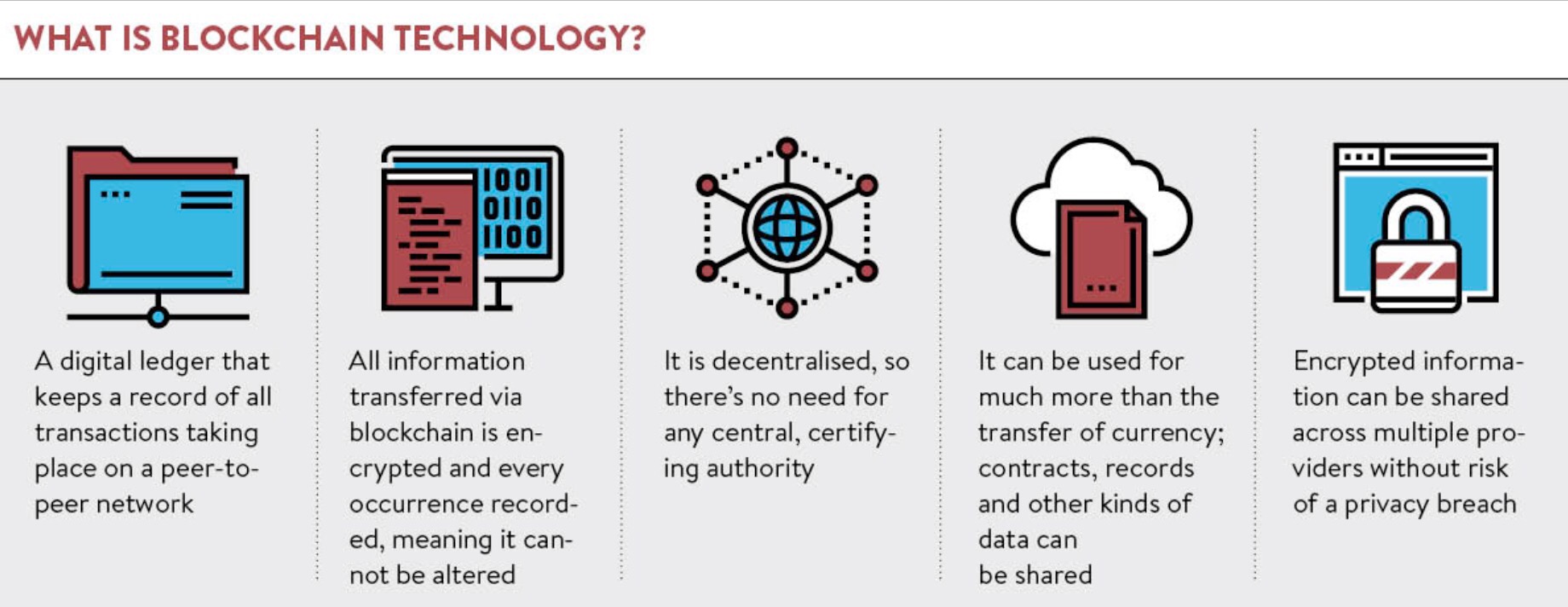

For a simple overview, the blockchain is the underlying technology behind things like Bitcoin.

It is essentially a distributed ledger; a list of all events and transactions entered onto it which is held simultaneously by everyone in the network.

Every time a new event or transaction is added to the ledger, this encrypts everything before it. This means that the data on the ledger gets more and more secure with every addition to the ledger. The ledger is both visible to all in the network and secure so that people can’t tamper with it.

As BlockGeeks put it in their introduction to blockchain:

By allowing digital information to be distributed but not copied, blockchain technology created the backbone of a new type of internet.

Every new piece of information added to this ledger is added as what we call a “block”. This block is mathematically encrypted and is approved to be added to the ledger via a series of consensus protocols; ways of approving additions and protecting against fraud or double spending without the need for a centralized authority.

Through this ledger, and with a bit of computer code, you can create what is known as “smart contracts”. These are a series of clauses which are added to the ledger and powered by computer code. When the clause in the ledger is met, the computer code activates and the next step of the contract is triggered. Like automating simple legal processes.

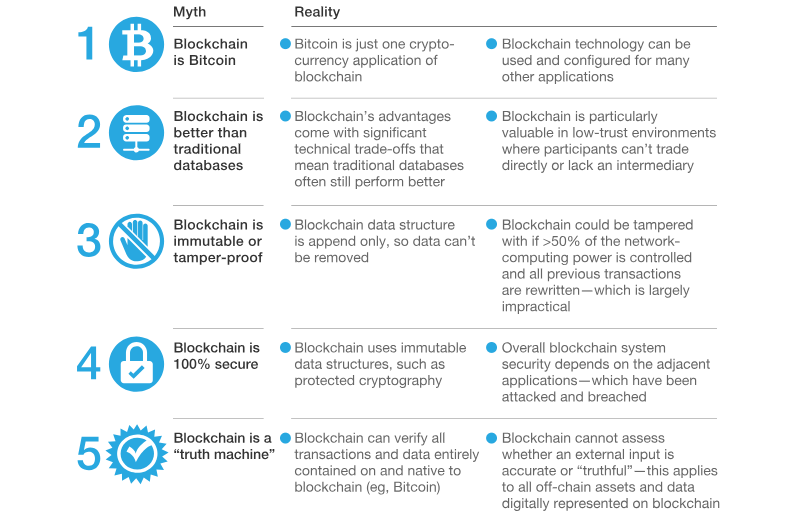

The report from McKinsey, discussed below, provides this easy to understand graphic covering a few myths of the blockchain:

There is a lot of excitement about the potential uses for this technology. Part of this excitement is driven by the digital tokens, or coins, which are built into these blockchain networks and the value they could hold. Yet, there’s plenty to be excited about in regards to application of the technology itself.

According to McKinsey:

Leading technology players are also heavily investing in blockchain: IBM has more than 1,000 staff and $200 million invested in the blockchain-powered Internet of Things (IoT).

It’s this practical purpose which I’m particularly interested in as it could change the way we do business or run our operations. But it has been slow going so far. Many blockchain based startups have raised money because they’re on the blockchain rather than because they have a great business, with McKinsey adding:

Unstructured experimentation of blockchain solutions without strategic evaluation of the value at stake or the feasibility of capturing it means that many companies will not see a return on their investments.

Nonetheless, through extensive research the report from McKinsey brings us a series of conclusions. These are the report’s three key insights into the strategic value of blockchain:

- Blockchain does not have to be a disintermediator to generate value, a fact that encourages permissioned commercial applications. So it doesn’t need to be a full 100% zero-trust use case for blockchain to add value. It can have positive applications before this point.

- Blockchain’s short-term value will be predominantly in reducing cost before creating transformative business models. McKinsey expect blockchain technology will streamline existing structures before creating successful new ones.

- Blockchain is still three to five years away from feasibility at scale, primarily because of the difficulty of resolving the “coopetition” paradox to establish common standards. Basically, companies need to both cooperate and compete. In a new environment with new structures, McKinsey believe this will take a little time to work out.

McKinsey’s primary strategic advice for companies wanting to enter into the world of blockchain comes in two forms:

- Identify value by pragmatically and skeptically assessing impact and feasibility at a granular level and focusing on addressing true pain points with specific use cases within select industries.

- Capture value by tailoring strategic approaches to blockchain to their market position, with consideration of measures such as ability to shape the ecosystem, establish standards, and address regulatory barriers.

Or, simplified, stop thinking of blockchain as a silver bullet and instead address business concerns the same way you would when launching any startup, new product, or new services. Don’t just create blockchain applications for the sake of it, create them where they make business sense.

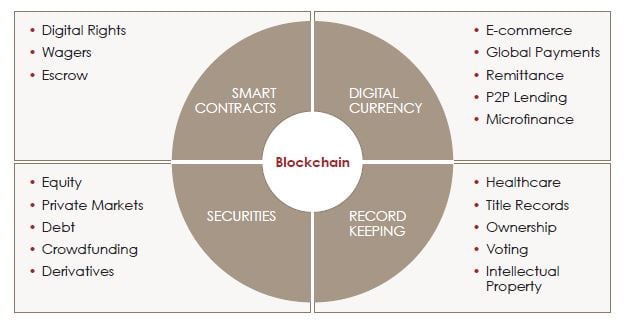

5 use cases where the blockchain could thrive

We know the concept of the blockchain now, but we’d quite like to find some immediate use value.

In theory Blockchain technologies could fit in place of certain existing platforms to better provide services, or they could be incorporated into various flows to remove a trust-oriented middleman.

This second option is perhaps more interesting as it paints blockchain as an automation technology which doesn’t just change things technologically but changes the material ways in which we go about doing things.

A smart contract could replace a legal go-between, for example.

Whole business processes could possibly be automated and executed through the blockchain with multiple stakeholders being involved. But we’ll come to that in more detail.

In the meantime, we’ll pull from the Economist to look at 5 key use cases where the blockchain either could be implemented, or is already being implemented – often a little of both.

Smart contracts change the way people make agreements

We’ve already mentioned smart contracts, but there’s a lot of excitement around their potential uses.

The Economist quotes Chris DeRose from American Banker:

[S]elf-automated computer programs that can carry out the terms of any contract… it is a financial security held in escrow by a network that is routed to recipients based on future events, and computer code.

So these smart contracts could theoretically automate large amounts of legal practice via their integration into agreements. Now, replacing legal professionals is probably considerably harder than writing a couple of bits of code, but there is clear potential in the concept.

The making of day-to-day agreements via smart contracts could come sooner than we think. Bike rental service Slock.it, use smart contracts to unlock bikes for rent once both parties have come to an agreement via the smart contract. It can also be used to unlock doors to Airbnbs or other Internet of Things style approaches; the renter’s mobile phone can act as the key.

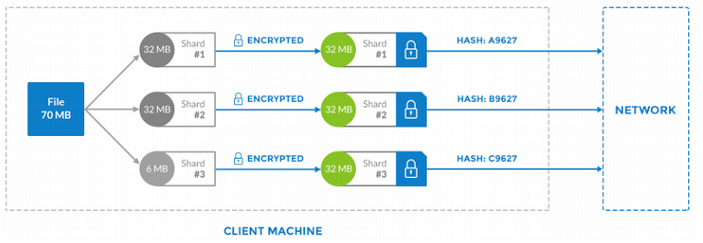

Cloud storage with native encryption

Blockchain allows you to do decentralized cloud storage by storing your materials on the computers of other people around you. The idea is that you’ll earn tokens (cryptocurrency) through storing these materials on your unused hard drive space.

Shawn Wilkinson, founder of Storj, describes it as:

Considering the world spends $22 billion + on cloud storage alone, this could open a revenue stream for average users, while significantly reducing the cost to store data for companies and personal users.

It’s basically Airbnb for your hard drive.

Storj is apparently launching early 2019 and other competitors like Filecoin are around for you to sign up to their early mining programs too.

It appears people are eager to get on board the blockchain storage.

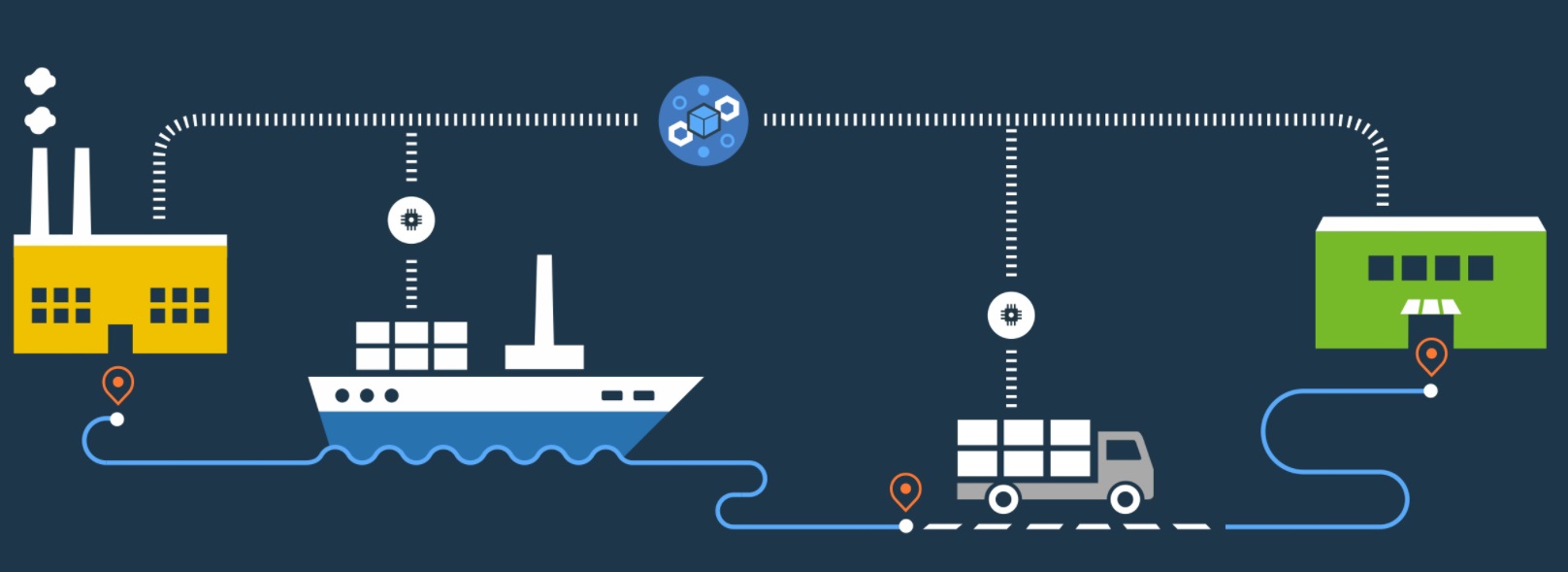

Supply-chain accountability via the ledger

Knowing where something in your supply chain came from is a very important thing. This helps ensure quality and protects your business against other people’s poor choices.

The idea behind using the blockchain for this would be that the ledger on the blockchain provides a transparent and encrypted way to securely make sure you’re buying what you believe you’re buying.

Phil Gomes says on Edelman Digital:

Most of the things we buy aren’t made by a single entity, but by a chain of suppliers who sell their components (e.g., graphite for pencils) to a company that assembles and markets the final product. The problem with this system is that if one of these components fails ‘the brand takes the brunt of the backlash.’

The Economist lists Provenance and Skuchain as up and coming players in a blockchain-enabled supply-chain tracker industry.

According to CoinDesk, Ant Financial – a payments affiliate of Alibaba – is in the process of launching a blockchain-built tracker in conjunction with the Chinese city of Wuchang. The brand of rice from the city is highly sought after but is often diluted with poor quality rice from other locations. Ant Financial and the Wuchang clan are going to collaborate in order to protect their neck and triumph. Blockchain is the method, man.

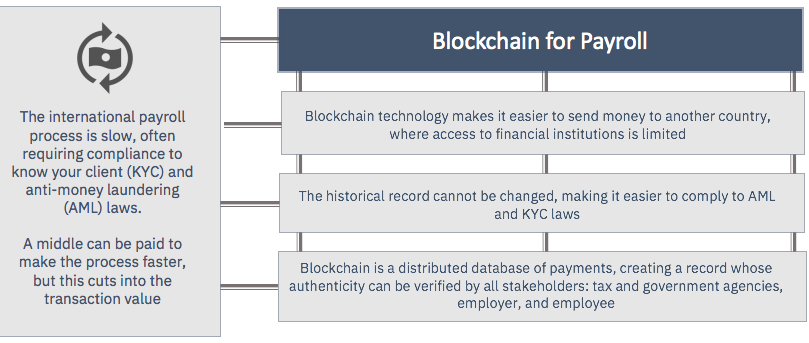

An introduction to blockchain for employees via payroll

As blockchain technology is part and parcel of the cyrptocurrency movement, and that seems to be where all the rage is, it’s probably no surprise to hear of the blockchain replacing use cases of currency in this list.

Geoff Weiss, writing for Entrepreneur, makes the case for token payments to employees as:

If your company regularly pays wages to international workers, then incorporating Bitcoin into the payroll process could be a major cost saver.

Which makes sense. Cryptocurrencies could be used to pay workers in this way, and if the company is a blockchain one and the tokens are issued by the company then workers would see their asset values raise with the success of the company, provided they were able to hold on to some of their tokens.

Maybe optimistic… but there could be some future in it.

The Economist quote Bitwage in saying it will:

…circumvent the costly fees associated with transferring money internationally, as well as the time it takes for such funds to move from bank to bank, payments made via Bitcoin can save both money and time for employers and employees alike.

As use cases go, this one is partly off the ground. The only issue currently might be the price instability of Bitcoin itself, however there could be some ways round that.

Decentralize and democratize with the blockchain

So, there’s this thing called Delegated Proof Of Stake (DPOS) which people are excited about insofar as democratic functions goes.

BitShares describes it as:

DPOS leverages the power of stakeholder approval voting to resolve consensus issues in a fair and democratic way. All network parameters, from fee schedules to block intervals and transaction sizes, can be tuned via elected delegates. Deterministic selection of block producers allows transactions to be confirmed in an average of just 1 second. Perhaps most importantly, the consensus protocol is designed to protect all participants against unwanted regulatory interference.

The whole process is somewhat complicated, but the long and short of it is that there are a series of decisions which need to be made and technology sets automatic parameters and executes the decision making in a way which is publicly accountable through the ledger.

The hope many have moving forward is that blockchain tech could make activities like electronic voting safer and more effective.

According to the New Scientist, a US electronic voting machine can be hacked in less than 90 minutes. Blockchain technology faces challenges in securing anonymity in regards to votes while also delivering results, but these challenges can be overcome and could potentially help to uphold democratic rights in broader society.

According to the World Economic Forum, while discussing a new blockchain-powered app called Sovereign:

The first test of Sovereign allowed users to vote on an unofficial deal between Columbia and a rebel group. Each voter was given 100 votes they could allocate as they pleased across the seven main aspects of the agreement.

Following the end of the voting process, the deal was rejected — just like it was during the official referendum — but Sovereign revealed there was only one aspect of the deal people were truly unable to support. This revealed the app’s ability to provide insight that isn’t available through traditional yes/no votes.

A secure voting process which is able to glean a deeper understanding of voters’ concerns and wishes would be a big step forward for empowering democracy.

Sometimes people’s wishes are more complex than a simple yes or no. This kind of approach would help politicians to make policies based more accurately around democratic will instead of having to rely on small sample polling data to make sense of the binary choices presented in traditional referendums. Brexit, anyone?

How the blockchain could be utilized in business process management

So we can now see some of the advantages which the use of blockchain technology may bring to different industries.

But to what extent does this translate into business process management?

You might say:

What if every Process Street checklist which was ran recorded every change or entry to it onto a ledger? That would provide transparency as to revision changes and who had interacted with the checklist.

And you would be correct. The thing is, you already record that information as a company in the database logs anyway. In Process Street, you can use the Template Overview to see the important information which had been entered into the checklist.

That kind of change can be offered by companies already with strong enough security that the extra cryptography makes little real world business impact.

That use case doesn’t seem to provide a big enough competitive advantage, if any, for a company to progress with it.

However, the world of business process management is filled with use cases and with different kinds of stakeholders who seek out varying levels of service.

Can the blockchain find itself a place within this sea of potential value?

A collection of researchers, writing in the ACM Transactions on Management Information Systems journal, believe the answer to this question is “yes”.

The 2018 paper, titled Blockchains for Business Process Management – Challenges and Opportunities, shared with me by one of the authors Marlon Dumas, outlines a series of key points and evaluates them critically in the process.

Blockchains for business process management: The case for blockchain

- Zero-trust allows for companies to collaborate on processes. One of the traditional difficulties in process management has been inter-organization processes where different companies work together on the same process. The blockchain would mean there was no centralized power in this relationship. This means two business entities would be able to do business even without a trusted third party.

- Smart contracts can be assembled from inter-organizational process maps. The control flow and business logic from high level process overviews can determine the structure of a smart contract. Through connecting with web services, different moments in the process map can act as triggers for smart contract clauses.

- Payments or escrow services could be built in. Through the use of the cryptocurrency potential within the technology, payments made directly or ones to be held in escrow can be done automatically.

- The public ledger helps minimize disputes. If all information is held on the public ledger then it is possible to see who did what when and trace problems to their root. This could minimize multi-stakeholder disputes through the open recorded history of the process and its transactions.

- Encryption could protect private information. With the use of the blockchain’s encryption capabilities, it would be possible to control what information was public on the ledger and also limit what information was visible to what participant.

Blockchains for business process management: Some immediate challenges

- Encryption could create difficulties for process mining. If you’re looking to create an as-is process map, you might use a process mining software to run through non-encrypted event logs to allow you to discover your current operational process or processes. However, with blockchain tech these event logs may be encrypted and not organized in a manner which allows for effective process discovery.

- The same problem hurts analysis. While the argument could be made that your process analysis has the potential for improvement via a view of your processes in the whole supply chain, there are other criticisms too. As with the encryption stopping process discovery, the same applies to process analysis of encrypted data. To protect your external security – advertised as a selling point of blockchain – you may damage your ability to understand your processes. Weakening the encryption could allow competitors to view your processes through transactions or reverse engineer your processes via smart contracts.

- Process adaptation or evolution is limited by zero-trust. The point of using the blockchain for this kind of exchange is that the parameters are defined beforehand and they have to be adhered to in order for a contract or process to continue forward. In real life, processes may have to be adapted in the wild. Blockchain solutions do not appear to confer any advantage in that scenario and may struggle more as the traditional guarantors of trust are not present.

Blockchain may give a niche advantage for inter-organizational business processes

It’s hard to judge whether or not blockchain will result in a revolution of business processes.

Partly, this is because most of the challenges of business process management are less about technology and more about people or organization.

Plus, many of the scenarios described above can to certain extents be achieved with currently existing technology.

In the paper, it talks about businesses collaborating with each other automatically in a marketplace facilitated by blockchain and executed by smart contracts. This is all well and good but automating what company you are buying from as some form of streamlined procurement presents a significant risk in regards to quality – regardless of whether the ledger looks good or not.

The paper presents a series of obstacles which currently exist for blockchain-powered companies, including throughput, latency, bandwidth, usability, security, wasted resources, and hard forks (decisions to change the way a blockchain platform operates).

In its current form, a blockchain solution doesn’t present too much that current BPM software or BPM tools don’t already provide. Process Street allows you to assign checklists to people outside of your organization, or even just assign tasks. There are many ways you could use the Process Street platform for business collaboration.

I imagine the specific use case most closely related to what is described in the paper would be large corporate bodies who value security and operational secrecy and seek to do business with other corporate firms internationally while skirting around regulations.

There may well be a great future in blockchain facilitated business process management, but that future is not now.

Have you implemented blockchain technology in your business? Are you looking for ways you could implement it in future? Let me know your thoughts, hopes, and concerns in the comments below!